The Volkswagen Disaster: Could Analysts See It Coming?

Volkswagen (VLKAY) share prices fell by more than 20% this week amid an emissions scandal that affects 11 million cars worldwide. It has triggered a critical question: Could analysts have seen it coming?

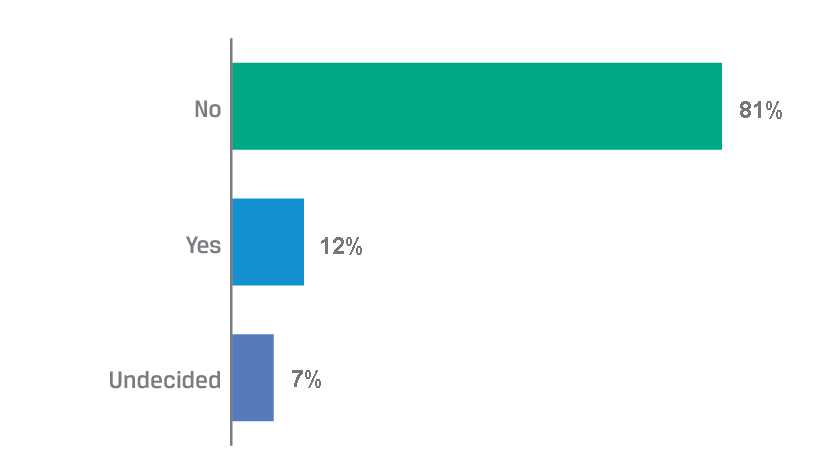

We posed this question to the readers of CFA Institute Financial NewsBrief. A clear majority, 81% of 826 respondents, said no, financial analysts cannot anticipate the risk of such losses through analysis of a company’s governance and internal controls.

Volkswagen’s share price suffered a large decline amid the US air-pollution tests scandal. Can financial analysts anticipate the risk of such losses by analyzing a company’s governance and internal controls?

The Argument for No

Analysts rely on publicly available information from companies, regulators, news media, rating agencies, and other sources. But what we are talking about in the Volkswagen case — to use the most polite adjective now employed by the news media — is deception. Deceivers try to avoid making their lies public. When the news comes out about such deception, it will always catch the market by surprise. You can see it with hindsight but not foresight.

James Macintosh argued in the Financial Times that investors need to go beyond box ticking and that analysts’ valuation models “must assess corporate governance.” Not everyone was impressed. “Great reminder after the fact. Any other insights into the past?” commented one reader.

Could the modern sustainability/environmental, social, and governance (ESG) movement have helped provide some foresight?

Foresight with Sustainability Analysis?

Some analysts have been arguing that integrating ESG issues results in more complete investment analysis and leads to better informed investment decisions. Clearly, the idea is not that one can predict specific events like the emissions scandal, but that one can judge the probability of such an event happening and act accordingly. When we recently surveyed CFA Institute members, 63% of respondents said that they analyze governance issues in investment decisions.

So why couldn’t all those analyzing the governance of Volkswagen see it coming, particularly the ESG specialists? They saw Volkswagen proudly touting its sustainability record on its website:

“The Volkswagen Group has again been listed as the most sustainable automaker in the world’s leading sustainability ranking. As in 2013, RobecoSAM AG again classed the company as the Industry Group Leader in the automotive sector in this year’s review of the Dow Jones Sustainability Indices (DJSI). Volkswagen is thus one of only two automakers to be listed in both DJSI World and DJSI Europe. . . . The review analyzed the corporate performance of a total of 33 automotive companies, seven of them from Europe. Volkswagen took pole position with a total of 91 out of 100 possible points.”

So why couldn’t this sustainability/ESG analysis do any better? It too relies on publicly available information. But why did 12% of our poll respondents choose to answer yes? What are they thinking?

The Argument for Yes

Bad governance produces bad outcomes, and it was public knowledge that Volkswagen has serious governance problems. Back in 2009, the Financial Times published a story, “VW Governance ‘Worst’ of German Blue-Chips.” And this is not an isolated account. For instance, in 2012, the Financial Times ran another less-than-complimentary piece, “VW’s Governance Regime Irks Investors.” There were many such reports in mainstream news.

Bad governance infects a company and makes bad things possible. Here I would quote a comment posted on the New York Times website by one reader in response to a news report on Volkswagen:

“I used to work on emissions control software for one of the Big Three. The engine control and emissions diagnostics software is incredibly complex. We had hundreds of software developers, calibrators, validation experts, etc., working on these efforts. If you worked on oxygen sensors or catalytic converters, or vehicle speed or really anything, the software would interface with dozens of other functional areas . . . there is simply no way that this effort didn’t involve a concerted effort by many individuals [emphasis added].”

It makes sense that deception on such a scale and for so long does not take place without an enabling culture, which in turn is nurtured by poor governance.

Indeed, there were also those who minced no words in forewarning about the grave consequences of poor governance at Volkswagen. Back in March 2013, Olaf Storbeck wrote for Breakingviews:

“Management theory and history of other companies show that this [governance] structure is a recipe for disaster. VW’s own story supports this case. In the early 1990s, it plunged into an existential crisis. A decade later, the company was rocked by a compliance scandal, involving prostitutes and luxury trips for the members of the workers’ council.”

Did he say “a recipe for disaster”? Bingo!

Still Not Convinced?

Some of us may still be skeptical that one could anticipate such disasters ahead of time. After all, you can always find some people forecasting catastrophe for some companies based on one reason or another. The future is bound to make some of them look prescient.

The point is that it was public information that Volkswagen had serious issues with its governance. The analysis that was proven right about Volkswagen has been proven right for the right reason. It was, of course, not possible to predict this particular scandal, but it was possible to judge that over the years, the governance issues at Volkswagen would cost its investors — and would cost them big. Analysts could see that coming.

If you liked this post, don’t forget to subscribe to the Enterprising Investor.

All posts are the opinion of the author. As such, they should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of CFA Institute or the author’s employer.