Do You Know What XBRL Is? A Majority of Survey Respondents Do Not Know

Despite the fact that eXtensible Business Reporting Language (XBRL) is the global standard for exchanging business information between financial reporting systems, a recently published CFA Institute survey showed that 55% of respondents* did not know what it was.

Awareness and Use of XBRL

In the survey, we first asked members which financial reporting attributes were important to them. We asked them to rank the importance of the following attributes: comparability, timeliness, reliability, consistency, and granularity.

Not surprisingly, respondents believed that all these attributes were important, with reliability being most important.

The next question was about the member’s level of awareness of XBRL. As shown in the following chart, 55% of respondents remain unaware of XBRL and 35% were aware but not up-to-date on its usage in financial reporting; together that comes to a whopping 90%.

Of those aware of XBRL, the highest proportions agree that XBRL-tagged interactive data will significantly improve their ability to increase the timeliness of the valuation process and their ability to upload company data into their financial analysis models.

More than three-quarters of respondents (77%) rated tagged information for all companies across a meaningful set of annual and interim periods as important for their use of XBRL-filed information.

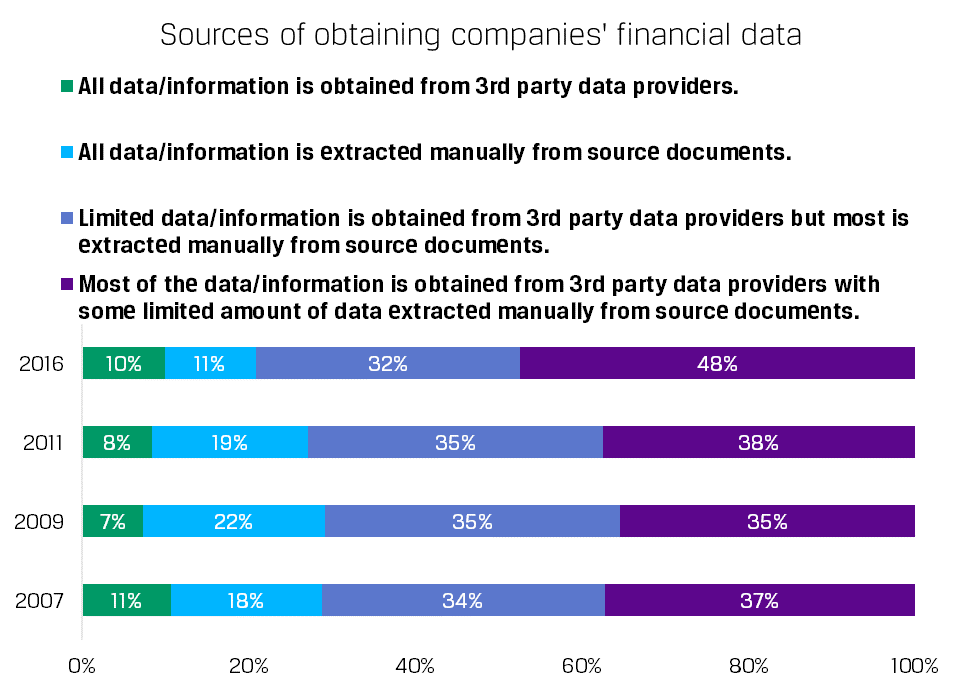

We then asked about the sources of obtaining company data, and the results were fairly consistent with previous years. As shown in the following chart, 48% of respondents obtain most of the data they use in their analysis of companies from third-party data providers, with a limited amount of data extracted manually. Ten percent obtain all data from third-party providers.

What the Results Are Telling Us

The primary story we are hearing is that companies are not using structured data as a communication platform, which is reflected in the fact that they are tagging only where they are required to and not beyond. They are tagging at the end of the financial reporting process simply to meet regulatory compliance needs. And it is also reflected in the poor quality of XBRL data that are submitted to regulators. Companies are not giving analysts a reason to embrace XBRL or to change their current practices. So, analysts continue to rely on data providers.

If companies changed their approach to the use of structured data, it could revolutionize financial reporting, as we have discussed in other posts. We will continue to work toward that end.

Read the full survey results to learn more.

*The regional distribution of the CFA Institute members who participated was as follows: 60% from the Americas region, 24% from the EMEA region, and 16% from the APAC region.

If you liked this post, consider subscribing to Market Integrity Insights.

Photo Credit: ©Getty Images/angelhell