European Equity Markets: A Crisis in Listings and a New Scheme for Private Capital Exchanges

European stock exchanges suffer from ongoing departures and a dearth of initial public offerings (IPOs) and other listings. Some important exceptions to this observation exist, notably in Sweden, but overall, the core economic functions of Europe’s exchanges — to raise capital from a broad range of investors, offer a venue for the exchange of ownership stakes, and value equity on the basis of liquid trading — are increasingly in doubt.

In a little-noticed acknowledgement of the crisis in public equity markets, the European Commission (EC), which initiates all financial regulation in the bloc, earlier this year committed to boosting secondary markets for private capital, including to support exits by investors in private companies. According to the EC’s most recent capital markets strategy, a more innovative approach should improve capital accessibility for smaller companies and offer private investors opportunities to engage with high-growth companies where public listings are not yet an option. In designing a scheme for the intermittent trading of private company shares, the EU regulators are bound to look at the United Kingdom, where unlisted companies can be traded outside the public markets since last year.

This is a surprising new direction. EU policy to date has focused squarely on making public exchanges for listed equity more liquid and transparent. Regulators generally presented IPOs as the culmination of the so-called funding escalator, as young companies progressively access more-demanding investor classes and asset types.

Europe’s market for private equity exchanges is not working

At least four motivations are behind the EU’s upcoming initiative.

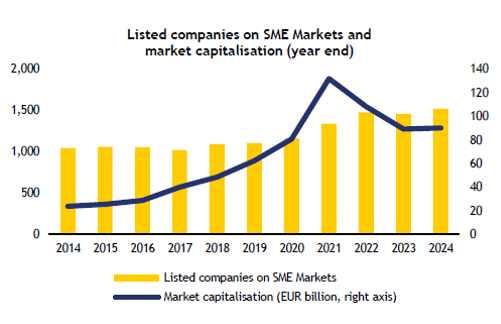

First, unlike in most other major advanced countries, primary equity market activity in the EU saw a sharp decline in 2025. A new assessment by industry body AFME suggests that in the first half of the year, EU IPOs fell to their lowest level since 2012. In three EU countries (Romania, Hungary, and Estonia), enterprises did not make use of market finance at all. As the chart below shows, equity markets dedicated to small and medium-sized enterprises (SMEs) finance (so-called junior markets) have seen a drop in capitalization and stagnating numbers of listed companies.

Source: Federation of European Securities Exchanges.

Second, financing constraints play a key role in holding back the EU’s startups and other young growth companies. A major new study of the EU’s venture and growth capital market shows that US markets typically provide four times more capital in comparable equity raising rounds. Capital raised cumulatively falls considerably short (according to this European Investment Bank study). Even though Europe generates a significant number of startups, difficulties in attracting lead investors to growth companies increasingly weigh on retaining innovative companies, thereby restricting productivity growth in the EU.

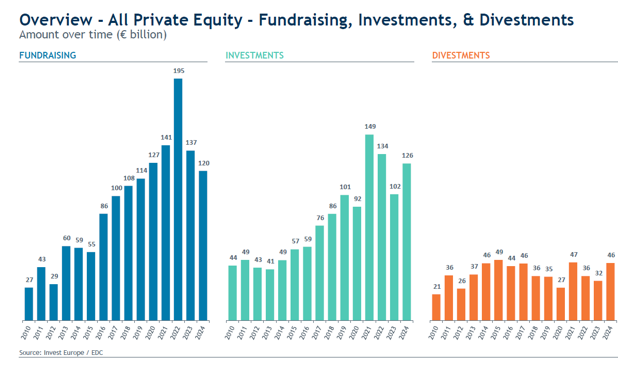

Third, the broader private equity sector in Europe, as elsewhere, has seen substantial growth in fundraising and investment over recent years. Assuming a lag of the typical investment period of roughly five to seven years, this should translate into commensurate growth in investment exits. But as the chart below documents (capturing the entire European industry), exits have been much more modest. IPOs are widely seen as too difficult, costly, or time-consuming. Alternative options, such as continuation funds, are now explored but are not an alternative to an ultimate exit.

Source: Invest Europe.

Finally, a similar concern has emerged for the ownership transition in private and family-owned SMEs. As Europe is rapidly aging, so are entrepreneurs in SMEs, where the ownership succession is increasingly in question. A study by German development bank KfW showed that 30% of entrepreneurs are older than 60 and underlined the role of financing constraints and attracting suitable strategic investors in identifying a successor.

An innovative UK scheme

In designing an alternative exchange for private equity and other ownership stakes, the EU can turn to one clear precedent from the United Kingdom.

Alongside a broader reform of the listing regime, the United Kingdom’s Financial Conduct Authority (FCA) in 2025 initiated a novel scheme for trading shares in privately owned companies: the Private Intermittent Securities and Capital Exchange System (PISCES). Two exchanges have already been set up under this scheme within a regulatory “sandbox” framework that shelters operators from certain legal risks.

The United Kingdom’s junior market Alternative Investment Market has seen a steady decline in listed companies and IPOs, resulting in greater price volatility and more limited liquidity. The new scheme is to provide exit options for private shareholders in companies that are not already listed. On PISCES, companies will control when auctions and trading windows open and who can potentially bid for shares. On the investor side, the scheme is limited to institutional and high net worth investors, though closed to retail investors. The United Kingdom’s FCA is clear that the scheme sets significantly lighter rules for disclosure and transparency than public markets would. Also, insider trading is not prohibited (the market abuse regime does not apply), though market manipulation is.

Navigating trade-offs

The EU should now update its rules for exchanges and trading venues to improve equity financing for startups and growth companies.

Overall, the EU approach to establishing an alternative model has been more cautious than that of the United Kingdom. Regulators have deliberately set high standards for exchanges and other trading venues with the aim of fostering price discovery and sound corporate governance, and based on scrutiny by a wide group of investors. The 2024 EU Listing Act aimed to simplify the process of going public for small firms, for instance with streamlined prospectus requirements and the option to define different classes of shareholders (see an assessment here).

But an additional venue for capital raising and secondary trading outside the public markets might now be needed. This could build on the experience with the United Kingdom’s private capital exchange (which itself is open to EU companies).

A platform could be defined as a new type of Multilateral Trading Facility under the upcoming revision of the EU’s capital market law (MiFID II):

- Widely accessible for all SMEs not already listed in the EU or elsewhere

- A light set of core disclosures, possibly augmented, depending on the rules of the operator and minimum governance safeguards as a precondition for admission to the platform

- Should the safeguards under the EU’s market abuse (insider trading) rules not apply fully, an obligation on sellers to disclose all material information

- Limited restrictions on the investor base (institutional investors and retail investors upon request, enabling SME ownership transitions)

- Periodic trading and auctions as determined by the operator

- Transparency on prices and valuations, for instance through aggregate reporting following a trading window

- Direct supervision by the European Securities and Markets Authority, as a significant trading platform with cross-border activity

Reforming the EU’s trading sector

A new type of platform would come on top of the already highly fragmented trading infrastructure in the bloc, which features more than 300 regulated markets and other trading venues. Ongoing efforts in consolidation and strengthening liquidity in the EU’s trading infrastructure should not be derailed.

A new private capital exchange would offer lighter transparency requirements, irregular price fixing based on more intermittent trading, and a restricted investor base. This could undermine incentives for firms to adopt the demanding standards of a listed company. Corporate insiders, such as managers, would be able to take on ownership stakes, and private equity fund managers could become more prominent.

These trade-offs now need to be confronted. Given the limited scope for trading of private equity finance, private exchanges are unlikely to usurp public markets in the near term. Yet as investor activity increasingly shifts away from public markets and companies opt to stay private, alternative venues are needed for access to growth capital.