Cummins: Catching a Bid ― Should You Chase It?

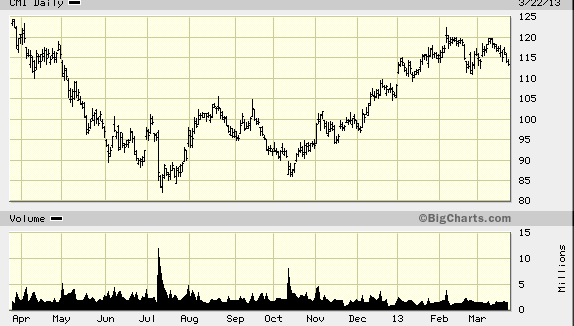

The shares of Cummins (CMI) have traded 17% higher (12% net) over the past three months, and our institutional clients are starting to ask what we think of the name. Stocks move for different reasons, but the fundamental driver is always tied to change in outlook ― such as an improvement or deterioration or an increase or decrease in risk. In recent weeks, machinery stocks have “caught a bid,” which is institutional investor lingo for “moved up a lot.” (If you are male, single, and in your 20s, you should use these words in financial district bars because they will increase your odds of dating success, I promise.)

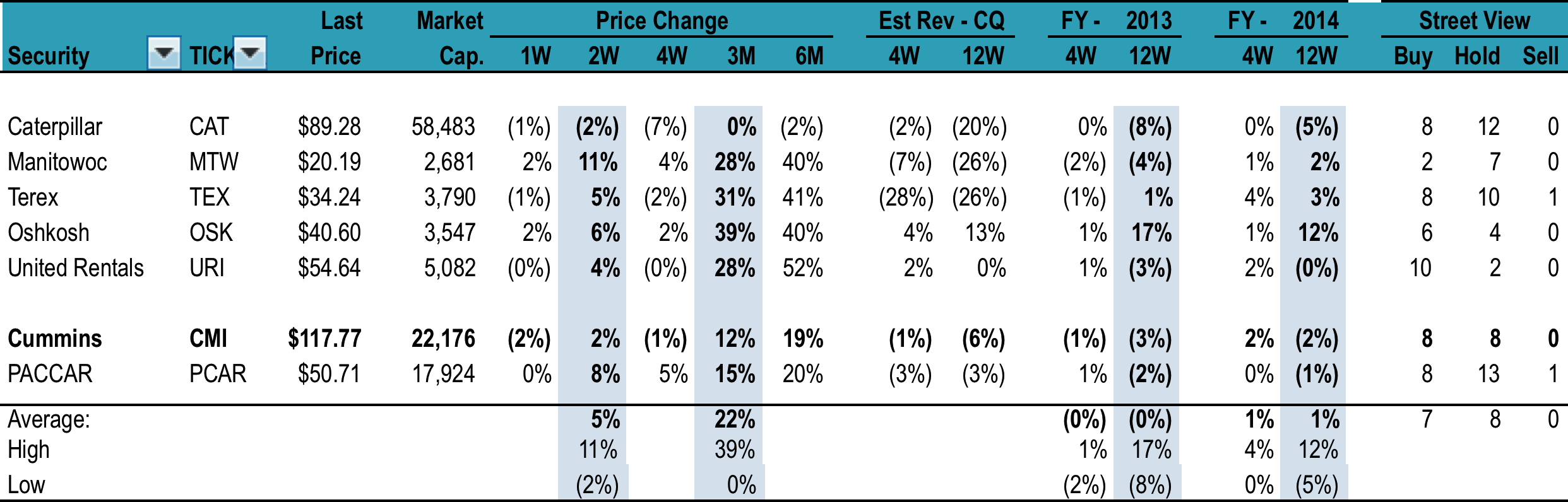

But let’s stay focused on making money; first, let’s dive into Cummins and figure out what to do with the stock. As usual, there is a lot of noise. Last week, four “name” sell-side firms confirmed or changed an estimate, rating, or target on Cummins, so in theory, you can just listen to Wall Street. Unfortunately, at three of the four firms the analyst has covered the sector for less than two years.

Should you buy Cummins? In our view, Cummins won’t make you rich or kill you. The average Wall Street price target is $130 and implies 15% upside plus the 2% dividend yield. The questions you need to answer are:

- Why has the stock moved? Is it the market, the sector, or a company-specific issue?

- What triggers, events, or factors will move the stock higher?

- What are the risks?

- Do I have better alternatives ― either more upside for the same risk or less risk for the same upside?

First of all, the market has risen 9% over the past three months, driven by “risk on” investing after the last-minute deficit ceiling deal in January, optimism about China, and improving data points from construction markets (both the Architecture Billings Index and residential construction). That optimism has flowed through the broad industrial sector: The S&P 500 Industrial Select SPDR (XLI) is up 9% as well. Within industrials, the hot subsectors are commercial aerospace and machinery.

Stocks always move on changes in expectations. Let’s dive into reality — something often lost by those of us who stare at quotes all day.

Machinery stocks are up 22% on average since late December, led by construction equipment stocks, cranes, aerial work platforms, and equipment rental, which have risen 28–39%. Caterpillar is the exception because of a glut of Chinese excavator inventory and a mining slowdown.

There is nuance here; note the rising quarterly estimates at Oshkosh Corporation (OSK) and United Rentals (URI) as well as the full-year 2013–14 forecasts. This rise is being driven by strong demand for aerial work platforms (such as these) tied to increased construction activity in North America.

Conversely, Manitowoc Company (MTW) and Terex Corporation (TEX) estimates for the upcoming quarter and for 2013 have been cut and 2014 estimates increased. This is where outlook meets reality; new $20 million cranes don’t just fly off the shelves.

One of the great things about being an analyst is that your “out year” forecast doesn’t hurt you; we can yak until the cows come home (or right before, when we adjust our numbers). But the next quarter is reality. And yes, I too have been guilty of making these adjustments.

Source: Langenberg & Company

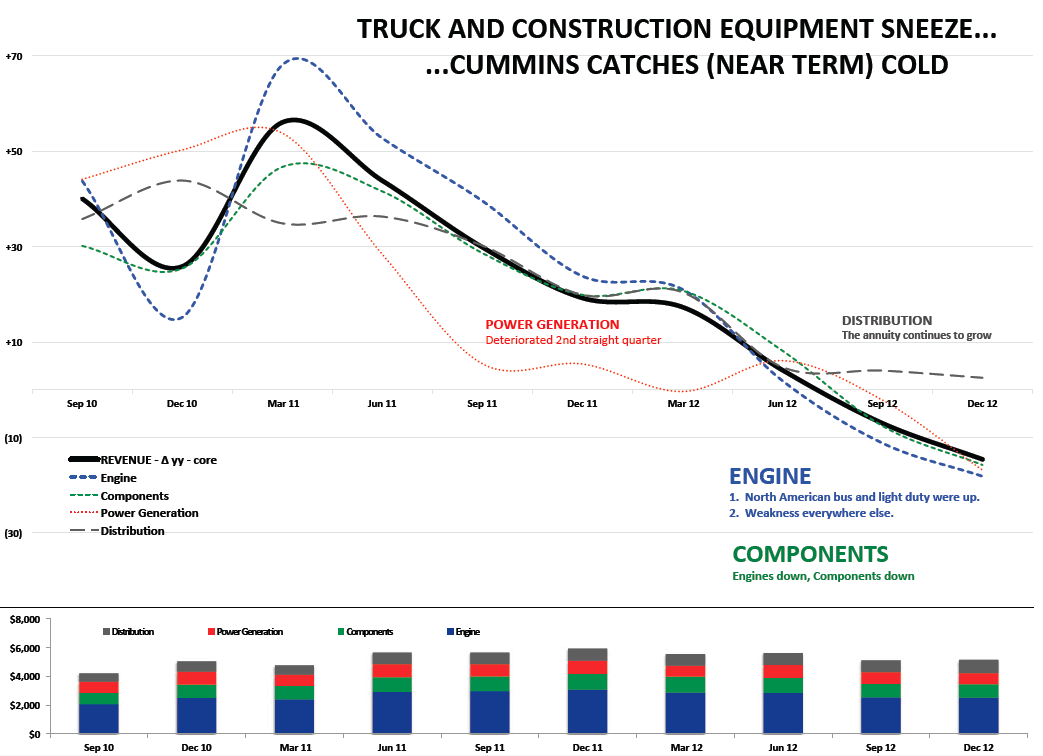

Cummins makes money by selling engines for big trucks, little trucks, pickup trucks, mining equipment, excavators, and oil and gas. It also benefits from building and growing its after-market businesses and joint ventures with mobile equipment producers in Europe, China, India, and Brazil.

Many large customers have excess inventory, and as the chart shows, recent core growth has turned negative. Cummins, in turn, has cut production schedules.

As a result, buying Cummins is a bet on an eventual rebound in emerging markets and resource end markets.

You need to get the direction right, and then, it is about time and return versus risk. Conventional wisdom is to value cyclical machinery stocks on mid-cycle earnings, which is, in my opinion, a stupid concept in a sector where the same company can earn $6 per share in a good year and lose money in a bad year. I’ve seen bad timing prevent fund managers from capturing alpha time and again or drive sell-side analysts to downgrade too early because clients don’t want to buy, bonuses are going to stink again, and why have the hassle? That being said, while (some) clients benefited from our MTW call in 2011–2012, we do think the bumper crop of hold ratings right now is spot on.

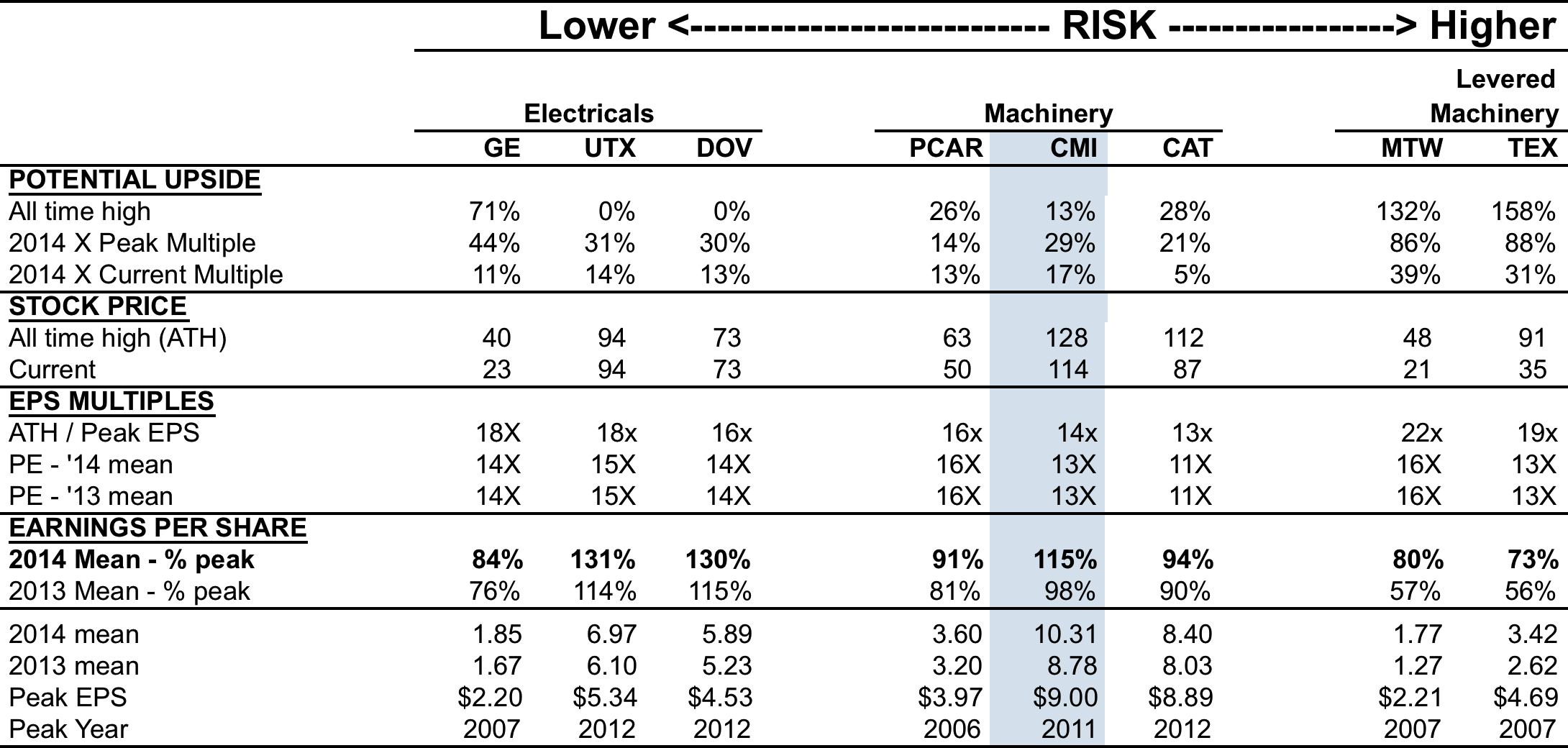

Cummins could be a good fit for moderate-risk investors who wish to participate in emerging markets. It is a different animal from the “heavy iron” customers it serves, and the company’s extensive, profitable operations in China and India in particular, including a growing after-market infrastructure, present long-term growth opportunity. Cummins also sports earnings stability (in the last 10 quarters, margin has held at about 12%, down from its 15–16% recent peak) and a pristine balance sheet (net cash position).

The average target price is $130, which we think is about right. Cummins is forecast to earn nearly 100% of peak earnings in 2013, despite slowdowns in multiple end markets, which underlies our view that earnings power is growing over time (increasing value) and not just recovering cyclically. If the 2014 consensus is correct and multiples are constant, we can expect a nearly 20% upside (including a 2% dividend). The other way to get at it is to use the “idiot check” of the prior all-time high, which suggests a 15% total return. Are there ways to make more money? In theory, both MTW and TEX can more than double and may do so, but it would be with high risk, including debt levels, lower earnings relative to the peak (56–57% in 2013, 73–80% in 2014), and end markets that have not really turned. Conversely, General Electric has $2.50 of earnings power but admittedly needs a U.S. power generation cycle to get there, which would, of course, help MTW and TEX. Are there ways to make a similar return with less risk? United Technologies Corporation (UTX) would fit that bill.

The takeaway is, Cummins won’t make you rich, but it won’t kill you.

If you liked this post, don’t forget to subscribe to Inside Investing via Email or RSS.