Investment Strategy: Rethinking Hedge Fund Indices

If you were to play word association with individuals in the investment industry using the phrase “hedge fund index,” the instinctive responses would be “survivorship bias” and “backfill bias.” The arguments for flaws in hedge fund indices, popularized by academics, are accompanied by an implication that hedge fund investors have not earned the returns that managers claim to have provided.

It’s as if hedge funds have been using anabolic steroids and academics are voting against their entry into the asset management hall of fame despite results that met investor objectives for two decades.

Creating a hedge fund index that reflects investor experience is certainly a challenge, but the assertions made in the academic research point fingers at the wrong issues. I find it frustrating to hear the same refrain when it isn’t quite right, so I thought it would be worthwhile to set the record straight.

Getting Up on the Wrong Side of Bed

Academic studies that highlight data biases in hedge fund indices all start with a false premise that renders irrelevant conclusions1. This premise is that an equally weighted hedge fund index can serve as a representative proxy for investor experience. Any conclusions that follow, including those proclaiming that hedge fund investor returns are overstated, are thus unproven. In technical terms, this methodology is called “garbage in, garbage out.”

Let’s start with first principles.

The purpose of constructing an index is to measure the aggregate experience of investors in a market. A properly built index must be asset weighted, representative, and investable.

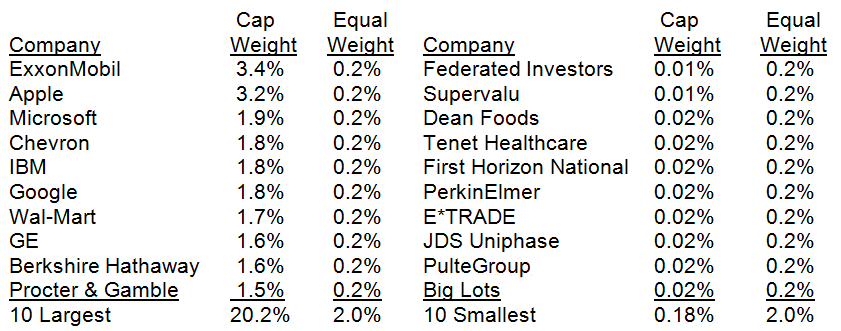

These prerequisites are likely impossible when constructing hedge fund indices. As a start, an example using the S&P 500 Index demonstrates the degree to which an equally weighted index does not reflect aggregate investor experience. The following table lists the 10 largest and smallest companies in the S&P 500 at the end of December.

The weightings of the most important constituents in the S&P 500 decrease by a factor of 11 when an equally weighted construct is employed. When “everyone owns Apple,” it would be silly to assess market returns by affording Apple the same weight as PulteGroup. Yet, that is just what most hedge fund indices do. In an equally weighted hedge fund index, the returns of a $50 billion fund carry the same weight as a $50 million fund.

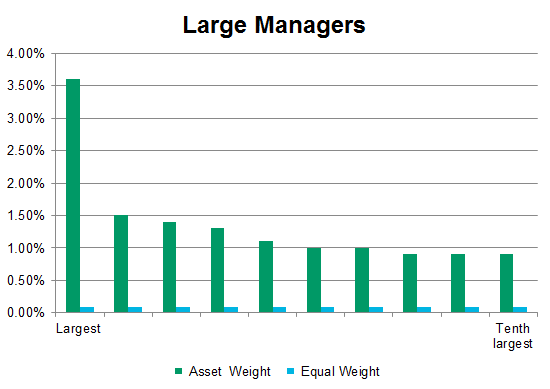

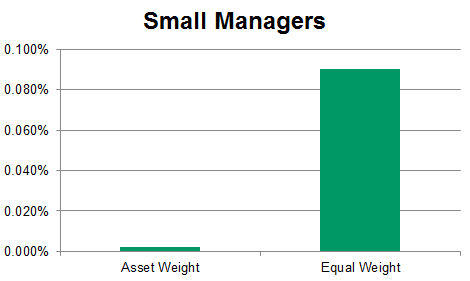

The following charts show just how differently a manager’s performance affects index performance under both methods. In the case of this index, the ten smallest funds are all the same size so the gap in effect is the same.

A quick peek at a representative set of the largest and smallest hedge funds in the HFR (Hedge Fund Research) Database demonstrates the concerns we would have if equally weighting the S&P 500. Although most casual observers of the hedge fund industry will be familiar with the brand names in the top 10, even serious professionals may never have heard of the smallest 10.4 The largest 10 funds included in the HFR Database manage $310 billion, whereas the smallest 10 oversee $0.5 billion, or 0.2% of that amount. In an equally weighted index, their returns count exactly the same.

The sole fact that equal weighted indices do not represent the experience of investors renders the vast academic research on these datasets inconsequential, if not meaningless.

Rebutting Proclaimed Bias

Even if academics started with a sensible dataset, their claims of survivorship bias are not unique to hedge funds and their cries against backfill bias are anachronistic. Survivorship bias is an active component of every well-constructed index. When the stock of the 500th largest company in the United States falls on hard times, it drops out of the S&P 500 and is replaced by an upwardly mobile company – a perfect example of survivorship bias.

Nevertheless, no one cries foul when survivorship bias occurs in the cap weighted S&P 500 because the weighting of the 500th largest company is an inconsequential 0.02% of the index. If stocks 450-500 counted the same as stocks 1-50 in the index and then fell off and were replaced by fast-growing ones, survivorship bias would matter much more.

Next, backfill bias immediately falls away when indices are calculated live. I would agree that any index whose historical data are changed or revised is suspect. However, those biases in hedge fund indices ended a long time ago, when the sponsors of indices first began compiling data. For years, index data have been run and reported on a monthly basis in real time, and backfill bias doesn’t occur.5

Given the obvious problems with equally weighted indices, it might come as a surprise that purveyors of an industry filled with incredibly smart people would perpetrate such a suboptimal practice. I suspect that the constructors of equally weighted hedge fund indices know full well that their products may not be representative of investor experience, but they recognize there is not much they can do about it. The largest funds have little to gain from sharing details about their returns and assets in the public domain.

Rather than survivorship bias or backfill bias, the real flaw in hedge fund index construction is one of robustness, resulting from the unavailability of the data that matter most.

Lack of Representativeness in Asset Weighted Hedge Fund Indices

Properly constructed hedge fund indices still struggle to collect data from many of the largest funds. This practical obstacle is especially relevant because the hedge fund industry is highly concentrated. Around 60% of industry assets are in the hands of just 85 firms. The only common hedge fund index that is asset weighted, the Dow Jones Credit Suisse Hedge Fund Index, has around 320 constituents and includes results from only 45% of the industry’s largest managers. The index may correlate enough to be representative, but the dispersion of returns across hedge funds is sufficiently wide that we really don’t know.

The absence of the largest funds from indices actually understates historical returns. Investors in aggregate notoriously chase returns, so it is reasonable to expect that the largest hedge funds today are those with some of the strongest track records historically. By excluding these significant and successful track records from hedge fund indices, the realized experience of investors is likely to have been better than that reflected in the Dow Jones Credit Suisse Hedge Fund Index.

Force Feeding Investability

Another challenge in constructing a useful hedge fund index is the requirement that the index be investable. Unlike stocks or bonds that are freely tradable and priced daily, hedge funds are private financial service companies that trade at book value by appointment. Some funds that are “closed” may open from time to time; others that are open may close. Some hedge fund firms have a single fund, whereas others have a series of funds. The complexity in aggregating the returns and assets of the largest funds in the formation of a proper index is compounded by the challenge of identifying which of those funds is investable and when.

To address this component of the equation, a few service providers have built “investable hedge fund indices.” In these vehicles, the index sponsors establish a fund that includes managers who agree to accept more capital into a pooled structure. Suffice it to say that very few of the largest funds participate in these products, and as a result, the investable indices will reflect aggregate investor experience only by chance.

A Better Approach

If industry participants really want to create a useful benchmark, a straightforward approach might be to aggregate fund-of-funds indices. Funds of funds oversee approximately $600 billion, representing around one-quarter of invested assets in the industry. Their allocations are instrumental in determining the relative size of hedge funds in the industry and are likely a good representative proxy for all investors. Any survivorship bias in a fund-of-funds index is unlikely to affect the returns of the hedge funds in which they invest. An index of funds of funds could meet the requirements of being asset weighted, representative, and investable.

Parting Thoughts

Allocators can’t rely on the existing hedge fund indices to serve as a benchmark for peer assessment in the space. Equally weighted indices are flawed by design, and asset weighted indices lack enough information to accurately assess what’s going on.

Academics who have cast doubt on history simply have it wrong. They start with a poor dataset and end with conclusions that have little merit.

The large size of the hedge fund industry and presence of allocators who report decades of strong track records strike me as speaking louder than flawed academic studies or poorly constructed indices ever could.

1. Walter Géhin and Mathieu Vaissié, “Hedge Fund Indices: Investable, Non-Investable and Strategy Benchmarks,” Edhec Risk and Asset Management Research Centre (October 2004). Géhin and Vaissié list 18 studies that report survivorship bias, instant history bias, or both. Every one of the studies examined an equally weighted hedge fund index, including widely cited work by William Fung and David A. Hsieh.

2. The 10 largest are the largest 10 managers in the InvestHedge Global Billion Dollar Club as of 2 October 2012 whose funds are represented in the HFR Database. Asset weighting assumes an industry size of $2.15 trillion.

3. Equal weighting is estimated based on 1,148 constituents of the HFR Database with assets under management in excess of $50 million, the minimum for inclusion in the HFRI indices.

4. I don’t know these funds myself, and they may be terrific. They are simply 10 funds at the $50 million cutoff that HFR uses to construct its index.

5. As an example, the asset-weighted Dow Jones Credit Suisse Hedge Fund Index took a hit of 3–4% in 2008 when the Madoff fraud came to light. As a presumably large manager, Madoff feeder funds had a substantial weight in the index.

If you liked this post, don’t forget to subscribe to Inside Investing via Email or RSS.

Please note that the content of this site should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of CFA Institute.