What Has the Financial Crisis Taught Us about Bank Performance Reporting?

The financial crisis provided a watershed moment for enhancing the transparency of banks. Financial institutions researcher Stephen Ryan of New York University has characterized the financial crisis as the single most ”teachable moment” in finance. To examine the effects of the financial crisis on bank performance, CFA Institute recently issued Financial Crisis Insights on Bank Performance Reporting (Part 1): Assessing the Key Factors Influencing Price to Book Ratios.

It is the first of a two part-study analysing the relationship between key elements of bank performance reporting (i.e., loan impairments, disclosed fair value, return on equity (ROE) and its components) and market indicators of value and risk such as price-to-book (P/B) ratios and credit-default swap (CDS) spreads. The study examines 51 mostly large, complex banks in the European Union, United States, Japan, Canada, and Australia from 2003 to 2013.

Explaining Low P/B Ratios

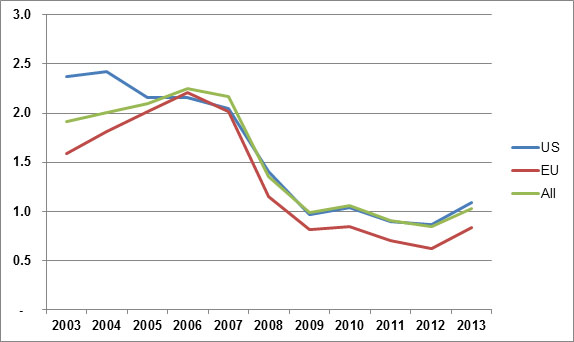

Part one of our study focuses on P/B ratios because it is a key valuation measure and commonly referenced by policy makers when gauging the financial soundness of banks. As shown below, the P/B ratios of many EU and US banks declined and have remained low since the beginning of the financial crisis — which begs the question, why? The P/B ratio reflects investor views on several factors, including future profitability, riskiness of future returns, and extent to which there is a perceived misstatement of bank balance sheets. The P/B ratio is also indicative of the incentives for banks to obtain equity finance at any particular point in time. Low P/Bs make it less attractive for banks to raise equity capital.

Declining P/B Ratios for Global Banks

Source: Bloomberg

Loan Impairments, Profitability, and Risk

Alongside bank profitability and risk, the key financial reporting information assessed in part one of the study is loan impairments (i.e., writedowns of the carrying value of loans due to reductions in expected recoverable contractual cash flows). That’s because loans are a key component of total assets for most commercial banks. Concurrently, delayed recognition of loan impairments is a well acknowledged problem that has led the International Accounting Standards Board (IASB) and the Financial Accounting Standards Board (FASB) to update their financial instruments accounting standards. Lack of timely financial asset impairments has also led the European Central Bank (ECB) and national regulators to do asset quality reviews and stress tests of bank balance sheets. In addition, the 2014 CFA Institute Global Market Sentiment Survey identified improvements in the requirements for banks to impair troubled credit holdings on a more timely and consistent basis as the second-most needed regulatory and industry action to improve investor trust and market integrity in local markets.

Key Study Findings

- Loan Impairment Effects on P/B (Market Valuation of Net Assets): Different analytical tests show the likelihood of delays in recognition of loan impairments leading to overstated reported balance sheets relative to the capital market valuation of these balance sheets. In the study, the evidence of lagging recognition of loan impairments is observed in respect to the allowance for loan losses and nonperforming loans, and is particularly pronounced for EU banks. This particular finding shows that the asset quality review of EU banks by the ECB is justified and will be beneficial for investors in revealing the true state of bank balance sheets.

- Loan Impairments Effects on ROE and Going Concern Value: Comparing the pre-provision income and net income for the sample banks shows that loan impairments significantly contributed to reduced overall net income at different junctures during the financial crisis (2008, 2009, 2010). The pre-provision income had a sharp drop in 2008 but improved significantly in 2009 and 2010. However, ROE dropped sharply in 2008 and has remained low in the periods thereafter. The contrast in pre-provision income and ROE trends in 2009 and 2010 reveals that impairments had a particularly significant effect on net income during the pinnacle years of the financial crisis. Their significant rise during the financial crisis means that loan impairments adversely affected the expected future earnings, risk premium on such earnings, and overall stock price.

- ROE versus P/B: Profitability measures (ROE) have an effect on the P/B; there is a positive association where higher (lower) ROE leads to higher (lower) P/B. Since the beginning of the crisis, there has been a significant drop in ROE alongside the corresponding decline in P/B. Furthermore, a year-over-year comparison of ROE versus the cost of equity shows that the cost of equity has exceeded the return on equity since the beginning of the financial crisis in 2008 (it was the other way round prior to that). This shows that the low accounting return and negative economic profit was contributing to low stock prices.

- Our results also show that the positive association between ROE and P/B became weaker during the financial crisis. This latter finding is likely to reflect that during the financial crisis, historical ROE became less relevant in predicting future ROE and stock price, attributable to the ongoing regulatory, structural changes that are bound to affect the long-term profitability of banks.

- Risk Effects on P/B: Risk measures (cost of equity, CDS spreads) showed a negative association with P/B — a rise in cost of equity and CDS spreads occurred during the crisis in tandem to the decrease in P/B. In addition, a comparison of the CDS spreads of similarly rated (investment-grade) EU banks and nonfinancial companies shows that there was an incremental spread towards the bank sector, hinting at an incremental risk aversion that translates to a relatively higher risk premium, lower stock price, and lower P/B for banks. We found that there has been a significant incremental average spread for sample EU investment-grade banks relative to their nonfinancial counterparts since 2009, when the Euro-sovereign debt crisis began to crystallize. For example, the incremental spread was 96 basis points (bps) in 2011 and 120 bps in 2012.

- Leverage and P/B: Excess leverage is a source of risk. Therefore, we assessed how leverage trends (tangible equity and Tier 1 capital) were related to P/B trends. We find that although leverage has improved, there is no discernible relationship between leverage and P/B. This finding, in part, reflects the limited potency of reported leverage as a signal of risk; part of the problem is the lack of comparability of total assets across jurisdictions.

Policy Recommendations

- Need for Fair Value and Amortized Cost Accounting: Recognizing that both the IASB and FASB have chosen mixed measurement (either fair value or amortized cost) for financial instruments, CFA Institute recommends requiring both types of financial instrument accounting in the long run.

- Improved Risk Reporting: We support enhanced risk reporting that has been proposed by several groups, including the Enhanced Disclosure Task Force. Improved risk reporting will help investors comprehend the complexity of the bank business model and underlying risk exposures.

- Improved Leverage Reporting: Excess leverage is a source of risk, and investors need to judge accounting leverage in addition to regulatory capital levels. Thus, investors should be able to compare accounting leverage for banks across jurisdictions, to better detect risk arising from leverage. Unsuccessful efforts to fully converge standards for offsetting financial assets under US Generally Accepted Accounting Principles and International Financial Reporting Standards were a missed opportunity to improve financial reporting for investors.

Part two of our study explores patterns of disclosed loan fair values, impairments across different countries, and how these correlate with such market-based measures of risk as CDS spreads.

If you liked this post, consider subscribing to Market Integrity Insights.

Great report, i wish we had more banks to look at from emerging markets.

Many thanks for your comment. I agree that including emerging market banks would allow the portrayal of a fully global picture of bank performance. That said, in our study we predominantly focused on the bank performance in countries that were most affected by the financial crisis, and also evaluated banks with similar structural features from several advanced economies.

Though there is some level of emerging markets coverage, because some of the large, global banks we analyze have operations in Asia, Africa and Latin America, there is certainly scope for analysis that includes banks from emerging markets.

Leaders of the five Brics nations agreed on the structure of a $50 billion development bank by granting China its headquarters and India its first rotating presidency. Brazil, Russia and South Africa were also granted posts or units in the new bank.

“Even with slowing economic growth in Brics countries, there are still plenty of opportunities for business, and the newly-created development bank will help those opportunities become reality,”.

We have the greatest amount to benefit because we’re partnering diplomatically and otherwise with some of the world’s most important emerging-market economies.

Kapil Chourasia

India

Great report!

In my view there is a relationship between leverage and P/B, as higher leverage favors higher ROEs (DuPont analysis), which in turn would lead to higher P/B…

tks

Thanks for your comment. Indeed, you make a valid observation. There is a relationship between leverage and P/B because, as you rightly note, bank returns were largely driven by excess leverage. However, this relationship can also be seen as a second order effect. This can explain why, in our analysis, the direct relationship between leverage and P/B was not readily observable through the period covered.

In the report we acknowledge that one of the shortcomings of ROE is that it is hard to discern, without a Dupont type decomposition, how much of observed returns are leverage-driven. A 2010 European Central Bank paper also discusses this shortcoming of ROE.

Vincent,

This is an excellent report and a commendable effort on the tricky empirical issues in your data.

Overall i think the results make intuitive sense although you correlation analysis suggests their may be a concern with regards persistence of your regressions’ dependent variable.

Such persistence can manifest as ‘dynamic panel bias’ which is something that cannot be capture using either fixed or random effects models.

Probably a minor issue but it may be something that you would like to include in your robustness checks going forward.

Barry Quinn

Barry — many thanks for your observations and feedback on the study. We will consider the econometric issues that you highlight in our future/continued analysis of bank reporting data.

Best regards,

Vincent

UN EXCELENTE TRABAJO DOCUMENTAL Y DE INVESTIGACIÓN, UN GRAN INFORME, UNA MAGNIFICA EXPOSICIÓN SOBRE DATOS Y ASUNTOS EMPÍRICOS QUE NO SON FÁCILES DE ARGUMENTAR, NI EXPONER, DE UNA MANERA TAN AMENA Y PRECISA. LA RELACIÓN ENTRE EL RATIO DE ENDEUDAMIENTO Y EL P/B, ES GENERADOR DE UN MAYOR INDICE DE APALANCAMIENTO FINANCIERO, QUE FAVORECE UNOS ROE SUPERIORES, QUE POR ENDE, DE FORMA DIRECTA, NOS LLEVA A OBTENER UN MAYOR P/B.- CREO QUE PUNTUALMENTE Y DE FORMA PUNTUAL SE TENDRÍAN QUE ANALIZAR LOS MERCADOS EMERGENTES Y LAS INSTITUCIONES FINANCIERAS PREPONDERANTES EN LOS MISMOS Y REALIZAR UN ESTUDIO PORMENORIZADO, COMO ASÍ MISMO LA INCIDENCIA DE LAS BALANZAS COMERCIALES EN LAS ECONOMÍAS MAS PROMINENTES Y SU RELACIÓN CON EL COSTE PAÍS Y LA PARIDAD DE SUS DIVISAS CON RESPECTO AL USD Y AL EURO.

Vicent, excellent article. With IFRS 9 delayed to 2018, we have missed an opportunity to align Regulatory approach to provisioning with financial statement with both moving to “expected” level which would speed-up the provisioning and alignment with financial market valuation