The Changing Use of Structured Data: Examples from around the World

My latest paper, Data and Technology: How Information Is Consumed in the New Age, takes a deep dive into how structured data (i.e., machine readable data) contained in regulatory filings in the form of XBRL (a type of structured data) is being consumed by investors and analysts. But, as XBRL International reports, XBRL is not used just for reporting to securities regulators. Possible uses for XBRL include reporting to lenders, tax authorities, and other regulating bodies. The following examples illustrate some ways in which structured data are consumed.

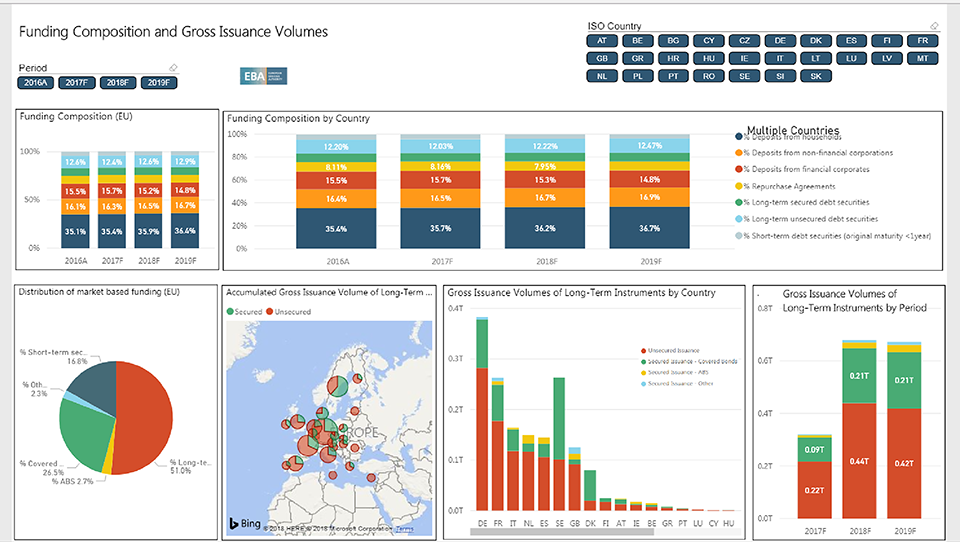

Example 1: European Banking Authority Produces Aggregate Data

The European Banking Authority now produces a remarkable range of aggregate data pulled from its holdings of EU-wide bank filings. For analysts within the banking regulator, the level of detail is exceptional, allowing them to select an area of interest and drill down within geographies, lines of business, areas of risk, and institutional groupings, and to further refine these results for individual institutions. If an analyst is interested in Non-Performing Loans in southern Europe, for example, this information is a few clicks away. The figure below provides an overview of the types of information available.

Example 2: Danish Business Authority Applies Machine Learning to Financial Statements

The Danish Business Authority (DBA), known as Erhvervsstyrelsen, collects XBRL financial statements from the approximately 240,000 private companies that operate in Denmark. It is exploring cutting-edge ways to apply machine-learning techniques to predict possible corporate failures.

DBA’s goal is to provide early warning information to entrepreneurs that their companies are exhibiting symptoms that could lead to restructuring, closure, or bankruptcy. It takes historical data about failed institutions, applies a range of techniques to their analysis, and then lets machine-learning algorithms develop patterns that can be matched against every other company’s data to locate similarities, and ultimately, risks. In its analysis, DBA is using hard financial measures such as solvency ratios, as well as softer data points such as changes in the lag between the end of the reporting period and the filing date.

Example 3: Ukrainian Authorities Take a Coordinated Approach to Reporting

Following the passage of new accounting laws (using International Financial Reporting Standards Foundation for disclosure), the Ukrainian authorities, including the Ministry of Finance, the National Bank of Ukraine, the National Securities and Stock Markets Commission (NSSMC), and the National Commission for the Regulation of Financial Services, agreed to a coordinated approach to reporting.

Financial statements prepared in Inline XBRL will be filed with the NSSMC and the data distributed to other agencies that need the information. The data will also be publicly available, improving transparency in this market. Entities affected by the changes include public companies, the financial sector, and a range of large enterprises. The changes are expected to come into effect in 2019.

The Ukrainian project seeks to develop a Standard Business Reporting (SBR)-style “report once” mechanism that lowers the administrative burden and reduces implementation costs by simplifying a range of data definitions and using a single portal to submit data to a number of different agencies.

Example 4: German Banks Use XBRL for SME Credit Assessment

The Deutsche Bundesbank (the German Central Bank), in coordinating with XBRL Germany, has been working with German banks to develop a small- and medium-size enterprise (SME) credit reporting system that leverages existing capabilities to generate XBRL financial statements for tax reporting. Commercial banks will be able to use these XBRL-formatted financial statements for credit and risk assessment.

The expectation is that wherever widespread private company financial statements or tax reporting are available in XBRL format, the private sector should leverage those reporting capabilities. The goal is to lower costs and the administrative burden for companies that need to finance their operations and to lower costs and risks for financial institutions.

Example 5: ING Discounts Loan and Credit Applications That Provide XBRL Financial Statements

In 2015, the Dutch bank ING began offering discounts on loan and credit applications for its SME customers in the Netherlands if they provided XBRL versions of financial statements through the Dutch SBR platform. When information is provided in this format, banks are better informed about their customers’ financial profiles.

By 2017, ING required its clients and prospective customers to adopt the standard or pay extra to file on paper.

Example 6: State of Florida Implements XBRL Reporting Requirements

In the United States, the state of Florida has more than 400 separate municipalities, including 282 cities. In accordance with US Government Accounting Standards, these municipalities prepare Comprehensive Annual Financial Reports (CAFRs), but their reports are in analog format.

Given the importance of municipal bond markets to the long-term funding of local and state infrastructure, Florida is moving toward digital government financial and performance reporting. The state will require the collaborative design and implementation of XBRL-based reporting from its municipalities. The CAFRs will be digital and all local governmental financial statements for fiscal years ending on or after September 1, 2022, will be filed in XBRL format.

If you liked this post, consider subscribing to Market Integrity Insights.

Photo Credit: guirong hao ©Getty Images/attribution