Berkshire’s Bottom Line: More Relevant Than Ever Before

In a 7 November 2018 Wall Street Journal opinion piece, “I Can’t See Berkshire’s Bottom Line: A New Accounting Rule Makes It Difficult For Investors to Make Sense of Annual Reports,” Donald E. Graham — chair of the board of Graham Holdings Co. (formerly Washington Post Co. and previously an investee company of Berkshire Hathaway) — echoes Warren Buffett’s criticisms regarding a recently implemented accounting standard on the recognition and measurement of equity securities.

As an investor organization that has actively participated in the debate over the accounting for financial instruments since the 2009 financial crisis, CFA Institute strongly disagrees with Mr. Graham’s criticisms. In our view, investors now have a more prominent and transparent display of the economics of the risks associated with the underlying investments. Berkshire Hathaway’s (Berkshire’s) net income is more relevant than ever before. Here’s why:

The New Accounting Versus the Old Accounting

The subject of the debate is US GAAP Accounting Standard Update (ASU) 2016-1, Financial Instruments — Overall (Subtopic 825-10), Recognition and Measurement of Financial Assets and Financial Liabilities, issued by the Financial Accounting Standard Board (FASB).The new standard, which became effective for public companies as of 1 January 2018, requires all equity securities for which management does not have control (e.g., 51% ownership) or significant influence (e.g., 20% ownership) be measured at fair value through net income. The FASB has allowed one exception that is applicable to companies with investments in equity securities without readily determinable fair values. Under that exception, securities are recorded at cost, less impairments.

Before the new standard, only equity securities classified based upon management’s intent as trading securities were recognized at fair value through net income. Under the previous guidance, the vast majority of equity securities were reflected at fair value through other comprehensive income and in equity as accumulated other comprehensive income. Although changes in fair value were included in other comprehensive income, and accordingly, comprehensive income, only dividends related to such instruments were reflected in net income. Also included in net income were the subjective impairment tests of management, which resulted in too-little, too-late recognition of permanent diminutions of value.

Under the new standard, investors have a direct line-of-sight into the change in fair value of the equity instrument because it goes through net income each period. Simply, the FASB reclassified the change in fair value from other comprehensive income to net income. Comprehensive income remains unchanged. Substantively, Berkshire’s true “bottom line,” comprehensive income, remains the same.

The Impact on Berkshire

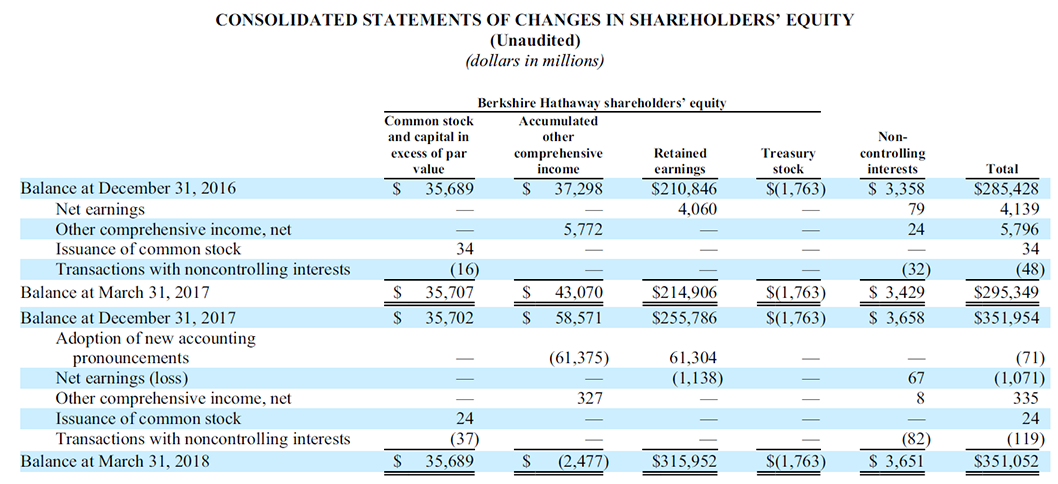

Berkshire adopted the standard effective 1 January 2018 and reclassified $61.4 billion (yes, billion) of unrealized gains, net of tax, from accumulated other comprehensive income to retained earnings. See Exhibit One. In the investment note, the unrealized gain on such securities was $95.3 billion. Tax affected at 21% this would appear to have been $75.3 billion. The reclassification also appears to include the stranded tax effects of approximately $14.1 billion — resulting from the change in tax rate from 35% to 21% — as $61.4 billion reflects a tax rate of approximately 36%.

Following the new standard, this reclassification reflects the fact the cumulative unrealized gains would have gone through net income if they had been accounted for under the new standard in prior periods.

Mr. Graham notes he can’t see Berkshire’s bottom line because of the volatility brought about by the change in the fair value of the instrument. Review of the 2018 quarterly financials indicates a new financial statement caption that clearly depicts the investment gains and losses and a footnote that illustrates the amounts that are unrealized gains and losses. That said, the financial statement caption is not readily reconcilable to the change in the cumulative unrealized gains in the footnote. Review of total comprehensive income from the prior year indicates that these unrealized gains simply moved from below (i.e., in other comprehensive income) to above the net income line. As expected, comprehensive income — the true bottom line — remains unaffected by the change in accounting principle.

Why the Bottom Line Is More Relevant to Investors

CFA Institute sees the issue differently than Mr. Graham and believes the income statement is more relevant than ever to investors.

- Berkshire’s Equity Securities Are Held for More Than Dividend Income.Most important, Berkshire does not hold these investments simply for dividend income. Heretofore, unless the securities were impaired, only dividend income was reflected in net income. Mr. Buffett holds these for “total return.” Total return includes the unrealized appreciation and depreciation of such securities and dividend income. Thus, the most meaningful measure of performance includes both elements of return. In Buffett’s 2017 Annual Letter to Shareholders he lists the 15 largest common stock investments with a market value of $170.5 billion and a cost of $74.7 billion, an unrealized gain of $95.8 billion, and notes the following (bolding by author):

Charlie and I view the marketable common stocks that Berkshire owns as interests in businesses, not as ticker symbols to be bought or sold based on their “chart” patterns, the “target” prices of analysts or the opinions of media pundits. Instead, we simply believe that if the businesses of the investees are successful (as we believe most will be) our investments will be successful as well.

That dividend figure, however, far understates the “true” earnings emanating from our stock holdings. For decades, we have stated in Principle 6 of our “Owner-Related Business Principles” (page 19) that we expect undistributed earnings of our investees to deliver us at least equivalent earnings by way of subsequent capital gains.

Our recognition of capital gains (and losses) will be lumpy, particularly as we conform with the new GAAP rule requiring us to constantly record unrealized gains or losses in our earnings. I feel confident, however, that the earnings retained by our investees will over time, and with our investees viewed as a group, translate into commensurate capital gains for Berkshire.

The connection of value-building to retained earnings that I’ve just described will be impossible to detect in the short term. Stocks surge and swoon, seemingly untethered to any year-to-year buildup in their underlying value. Over time, however, Ben Graham’s oft-quoted maxim proves true: “In the short run, the market is a voting machine; in the long run, however, it becomes a weighing machine.”

In his own words, Mr. Buffett acknowledges the stocks are not simply owned for dividends but also capital appreciation, albeit lumpy in the short-term.

- Income Statements Should Reflect Performance: Equity Security Decisions Are Integral to Valuing Berkshire’s Shares and Assessing Berkshire’s Performance. Some argue that such capital appreciation should be reflected in net income only when it is realized, or when the securities are sold. Until that time, the “performance statement” should not reflect the gains as they have not crystallized or converted to cash. That, however, is the purposes of the statement of cash flows.

CFA Institute supported the FASB’s revised standard, because investors consider the appreciation or depreciation of such significant holdings before their sale to determine the value of the organization and to assess the performance of Berkshire and Mr. Buffett. On 31 December 2017, the unrealized gains on equity securities accounted for nearly 17% (net of tax) of Berkshire’s total shareholder’s equity and they increase cumulative retained earnings by 24% (net of tax) when reclassified. Clearly this is a material consideration for investors in Berkshire’s common equity.

The issue is whether the income statement is meant to depict the change in the value of the organization during the period or the performance of the company — more specifically, the performance of management. Some argue the performance statement is not meant to reflect the performance of the equity market because it is not under the control or management of the company. In the case of Berkshire, for many, the performance of the company is inextricably linked to the performance of management — specifically the performance of Mr. Buffett and the performance of the equity market — given that the company’s business model is built on making such equity investments.

This debate over what the income statement is meant to measure is much of what creates the confusion Mr. Graham is experiencing. That said, the Berkshire income statement has been changed to clearly present these unrealized gains and losses as a separate financial statement caption.

To our mind, the issue at hand, is one of the objective of the income statement as well as the conceptual meaning of other comprehensive – an issue we have raised since its creation in the 1990s.

- Graham Illustrates Our Long-Standing Position: Investors Pay Less Attention to Other Comprehensive Income and Total Comprehensive Income Than to Net Income. We know from our many years of advocacy that investors pay less attention to “other comprehensive income” and “total comprehensive income” than they do to “net income”.

Even before the passage of Statement of Financial Accounting Standard No. 130, Reporting Comprehensive Income(SFAS No. 130), CFA Institute argued that other comprehensive income lacked a conceptual foundation in the accounting framework. In 2013, the FASB issued Accounting Standards Update 2013-2, Comprehensive Income (Topic 220): Reporting of Amounts Reclassified Out of Accumulated Other Comprehensive Income (ASU 2013-2). In it, the FASB changed the required presentation of other comprehensive income and comprehensive income such that this income would be presented more prominently as: (a) part of the income statement; or (b) a separate statement of comprehensive income presented after the income statement. The hope was that this change in prominence would increase attention paid to comprehensive income.

As shown in Berkshire’s Form 10-K and 10-Q filings, they, in fact, present a statement of comprehensive income – on the page following the statement of earnings. Unfortunately, Mr. Graham’s comments vividly illustrate the point made by CFA Institute. That being, investors don’t understand or pay close attention to other comprehensive income and accumulated other comprehensive income. It also highlights the change in prominence the FASB mandated in 2013 has not enhanced investors perception or attention. The true “bottom line” is comprehensive income, and as we have noted, this amount has not changed. The “bottom line” of which Mr. Graham speaks is that of net income, not the real “bottom line” which is total comprehensive income and remains unchanged.

- Berkshire’s Equity Risk Is Now More Effectively Communicated to Investors Through Increased Financial Statement Prominence. Graham argues that such presentation makes the financial statements less meaningful. Our view is that the presentation makes greater sense relative to other disclosures accompanying the financial statements, but still within the confines of the 2017 Form 10-K. Specifically, Berkshire acknowledges within the Risk Factors (page K-23) that they have higher than normal exposure, for an insurance enterprise, to equity risks:

Investments are unusually concentrated and fair values are subject to loss in value.

We concentrate a high percentage of the investments of our insurance subsidiaries in a relatively small number of equity securities and diversify our investment portfolios far less than is conventional in the insurance industry. A significant decline in the fair values of our larger investments may produce a material decline in our consolidated shareholders’ equity and our consolidated book value per share. Beginning in 2018, all changes in the fair values of equity securities (whether realized or unrealized) will be recognized as gains or losses in our consolidated statement of earnings. Accordingly, significant declines in the fair values of these securities will produce significant declines in our reported earnings. Since a large percentage of our equity securities are held by our insurance subsidiaries, significant decreases in the fair values of these investments will produce significant declines in statutory surplus. Our large statutory surplus is a competitive advantage, and a material decline could have a materially adverse effect on our claims-paying ability ratings and our ability to write new insurance business thus potentially reducing our future underwriting profits.

The analysis of equity risk within the Market Risk Disclosures section (page K-58) also highlights this significant equity exposure:

We often hold our equity investments for long periods and short-term price volatility has occurred in the past and will occur in the future.We strive to maintain significant levels of shareholder capital and ample liquidity to provide a margin of safety against short-term price volatility.

Indeed, results from declines [in fair value] could be far worse due both to the nature of equity markets and the aforementioned concentrations existing in our equity investment portfolio.

Presentation of the changes in fair value of these equity securities within net income draws increased investor attention to the risks disclosed elsewhere in the Form 10-K and the exposure they face as investors in Berkshire.

Analytical measures at year-end 2017 highlight the importance of these equity securities to Berkshire’s financial performance. In addition to the unrealized appreciation on such securities amounting to significant percentages of retained earnings and total shareholders’ equity, the fair value of the equity securities represented 33.7% of Berkshire’s insurance assets, 24.3% of total assets and 48.5% of total shareholder’s equity.

Excluding the volatility of these equity securities from net income eliminates communication of the very real equity market risk associated with an investment in Berkshire.

- During the financial crisis, companies had to make subjective judgments regarding whether securities were permanently impaired, whether and when to reflect such diminutions in value in the income statement and how to measure such impairments. Under the current model, investors — not companies — have to make such determinations. The old intent-based classification system with its subjective determination of impairment is no longer handled unevenly across companies. Under the new standard, all companies reflect the changes in value in the income statement contemporaneously without management judgment and with enhanced comparability for investors. This makes for more meaningful investment analysis.

- Accounting Differences Between Equity Method and Consolidated Equity Method Investments. Accountants are familiar with the three different accounting scenarios for varying levels of equity ownership. Berkshire’s operations and financial statements vividly illustrate the different accounting resulting from these varying levels of equity ownership and control and communicate the degree to which Berkshire can influence the operations of the business.

If a shareholder owns a majority of the investee’s share or possesses other rights that are indicative of control, the companies are consolidated. Berkshire’s financials highlight many such entities (e.g., Lubrizol Corporation; Precision Castparts Corp.; Shaw Industries Group, Inc.; Nebraska Furniture Mart). Kraft, over which Berkshire has significance as a member of an investment group, is accounted for using the equity method. These two types of holdings have a separate income statement caption.

For equity securities for which there is less than a 20% ownership, or no significant influence, this new standard more prominently reflects the value of the securities using the price Berkshire would need to exit these positions (e.g. exit price fair value). Although Mr. Buffett considers these businesses rather than ticker symbols, as noted in his remarks, the accounting for such appreciation in net income better reflects the difference in these positions than those over which Berkshire has greater influence or control and can contribute to the business operations. It is more accurate to reflect the change in the value of these investments in net income as it occurs rather than simply when management’s intent changes and the decision to sell is made. Reflecting the realized gains in net income at that time inaccurately portrays such earnings as current period events, when in fact, the gains may have accumulated over many years.

Now more than ever, the various methods of accounting for equity securities most accurately depicts Berkshire’s business model.

International Financial Reporting Standards

In the post-financial crisis era, the FASB and the International Accounting Standards Board (IASB) abandoned their efforts to reach convergence on the accounting for financial instruments. The accounting for equity securities under International Financial Reporting Standards (IFRS), may or may not be to Mr. Graham’s liking.

Under IFRS 9, Financial Instruments, issued in 2014, equity securities are accounted at fair value through the income statement much like US GAAP with two key differences. IFRS does not allow for the expedient provided under US GAAP for equity securities with unobservable fair values. It does, however, allow for the election of an irrevocable choice to recognize certain equity securities at fair value through equity (accumulated other comprehensive income) with no recycling of such appreciation or depreciation — into net income — upon disposal of the securities. Upon making this election under IFRS no capital appreciation is ever reflected in the income statement — only dividends. All realized and unrealized gains and losses are reflected in other comprehensive income. Furthermore, impairments are not recognized on losses reflected at fair value either through net income or through other comprehensive income.

Mr. Graham believes Mr. Buffett will hold his equity securities forever, so he might like the IFRS accounting better. Our guess is that the inability to ever recognize a gain or loss in net income would not be to his liking either.

CFA Institute has objected to this election under IFRS because the US GAAP accounting through net income is most appropriate, as we have supported above. Investors focus on the income statement and the risk and total return reflected in the income statement are important.

At the request of the European Commission (EC), The European Financial Reporting Advisory Group (EFRAG) engaged in a research project to examine whether it should be allowable to recycle gains and losses and to recognize impairments on those equity instruments recognized at fair value through equity. Many EC constituents, mostly non-investors, believe these allowances increase the relevance of the information. In Spring 2018, EFRAG issued a document for comment, Equity Instruments — Impairment and Recycling. The comments were summarized in a release in the Summer of 2018. Recently EFRAG issued its technical advice to the European Commission. Only two investors — the ultimate arbiters of what information is relevant to investment decision-making — provided feedback on the exposure document, EFRAG did not find support for recycling but did find support for impairment.

Challenge to Independent Standard-Setting Globally

CFA Institute believes it has made its position clear on the topic: fair value through the income statement is the most decision-relevant accounting and presentation. Although we don’t agree with the IASB’s election under IFRS, we believe IFRS and US GAAP standards — which have been under development for nearly a decade with extensive due process and current challenges brought about by Mr. Graham and the European Commission — through EFRAG — are counter-productive to independent standard-setting.

We find no evidence that Mr. Buffett, Mr. Graham, or Berkshire, for example, have provided formal feedback to the FASB during the numerous requests for public comment during this decades-long standard-setting process. Similarly, the constituents of the European Commission had innumerable opportunities to actively participate in IASB’s due process. After a decade debating the accounting for these instruments, we are concerned that Wall Street Journal opinion pieces and European Commission reviews seek to influence the outcome in an ex post fashion. Revisiting these issues because of the lack of desired outcome at this stage harms the independent standard-setting process.

Summing It Up

CFA Institute has devoted substantial resources to acting as a tireless advocate for investors in the improvement of financial reporting issues over the past 60-plus years. Advances in financial reporting to serve investors that Mr. Graham lauds in his opinion piece have been the result of the work of many CFA Institute members over time.

CFA Institute has been criticized during this long pursuit on behalf of its members and other investors for seeking reforms of all types including the balance sheet recognition of pension obligations, the expensing of stock options, the soon-to-be-recognized lease liabilities, and the recognition of financial instruments at fair value.

The CFA Institute 2010 comment letter to the FASB supported a much more significant expansion of fair value, a proposal the FASB did not advance. We issued a comment letter in 2013 to the IASB and FASB to reemphasize our views. We have provided our balanced investor focused feedback to the FASB and the IASB in a timely manner that was grounded in discovering the value of the business as promoted by the father of modern securities analysis Benjamin Graham (i.e., the other Mr. Graham of whom Berkshire’s Mr. Buffett was a student). If investors want to subtract the changes in fair value from their analysis, they are welcome to make such adjustments, but CFA Institute believes that the revised accounting provides investors with a better understanding of the risk, volatility, and valuation of Berkshire.

Image Credit: © CSA Images

It would be nice if we can have presentation examples in the article. too much jargon and write up doesn’t explain the impacts and presentation under new proposed IFRS standard