Equities versus fixed income: How ESG factors affect both asset classes

The content in this blog is based on a CFA-PRI survey of 1,100 financial professionals, mainly CFA members, from around the world, as well as workshops in 17 markets, as part of a best-practice report. For more information, see Guidance and case studies for ESG integration: Equities and fixed income.

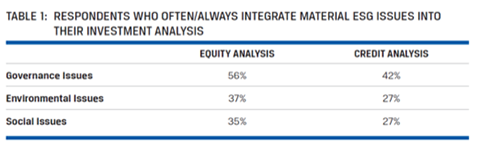

Fixed-income practitioners lag their equity counterparts when it comes to integrating ESG data into the investment process (see table X), reflecting a previously widespread view that ESG integration and fixed income are incompatible — a fading misconception.

Table X

It is fair to say that equities had a head-start on this front, given that the first application of responsible investment practices, mainly divestment and voting practices, were fundamental equity strategies. ESG integration in equities started gaining momentum at the start of the 21st century, and while ESG integration in fixed income is still in its infancy, it is expanding rapidly.

While fixed-income portfolio managers and credit analysts have traditionally been somewhat nonchalant regarding ESG, that is not to say it has escaped all radars. Indeed, some practitioners have been integrating ESG factors for quite some time, although few firms have been doing so on an ongoing, firm-wide basis.

Challenges to fixed income

One reason for the slow uptake of ESG integration in the fixed-income space is the lower level of active ownership in this asset class, while such a strategy is a strong driver of ESG integration in the equity world.

Unable to vote, bondholders find it harder to engage effectively due to limited access to management (for example, they don’t have a formal communication process such as an AGM). However, as noted by a participant at the UK workshop, it’s not that practitioners can’t engage with companies if they are bondholders; bondholders can and do have access to, and regularly meet with, management.

Even so, the absence of voting rights has created a perception that it is difficult to integrate ESG factors into credit analysis, with Dutch workshop participants agreeing that widespread knowledge of how to integrate ESG into bonds is lacking. Echoing this, “limited understanding of ESG issues/integration” was ranked as the top global barrier to ESG integration among fixed-income practitioners (see chart below).

Other challenges come down to the characteristics of fixed-income markets, with some participants in France of the view that fixed-income markets rarely price in ESG issues. One reason given for this is that those markets are relatively illiquid compared to equity markets, with bondholders therefore less likely to act on ESG issues and events. There is also the belief that traditional financial factors (such as interest rates and inflation) have an overriding influence on prices, resulting in ESG issues not getting the attention they merit.

Meanwhile, several European participants believe that ESG issues can have a bigger impact on a share price than on a bond price due to seniority. Because shares are more exposed to ESG risks than bonds, shareholders will lose their money before bondholders if a company goes bankrupt; thus, the impact of ESG data on fixed-income practitioners is cushioned. However, there would be a large impact on bond prices in such a scenario.Fixed-income practitioners must also deal with the fact they are operating in a bigger, more complex market, with a wider variety of instruments, maturities, and issuing entities.

ESG and fixed income are compatible

Despite these challenges, a point made repeatedly at several workshops was that fixed-income practitioners tend to be long-term investors, particularly pension funds and insurance companies. Therefore, ESG factors — which are also long-term in nature — are hugely significant to them.

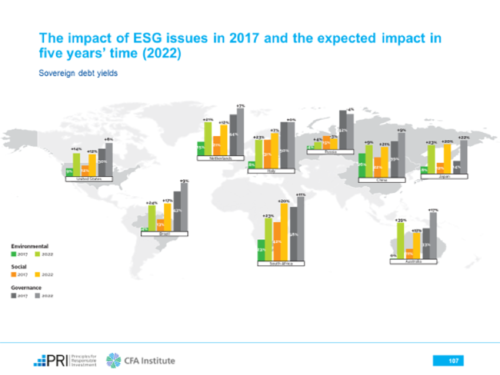

In fact, according to one practitioner in South Africa, ESG integration is more important in fixed income than equities.Because the former market is less liquid than the latter, when a major ESG incident does occur there will be a bigger impact on price, and the issuer could even default. Our survey showed that practitioners in all corners of the world believe that ESG issues affect corporate-bond and sovereign-debt prices, and that this impact will be even more visible by 2022 (see Figures X and X).

The misconceptions surrounding ESG integration in fixed income seem to have contributed to a knowledge gap among fixed-income practitioners. Workshop participants around the world agree that training is crucial to encourage greater ESG integration, including the pricing-in of ESG factors. This is already happening in response to increasing client demand for fixed-income products that consider ESG factors.

Contributing author: Justin Sloggett, CFA, Head of ESG Investment Research, UNPRI.

Image Credit: © Witthaya Prasongsin