CFA Institute Is Not Giving Up on the Convergence of GAAP and IFRS

Now, it is one thing getting to converged Standards. It is yet another is to keep converged Standards converged…keeping converged literature converged is oftentimes easier said than done.

Dr. Andreas Barckow, Chair of the International Accounting Standards Board (IASB)

Investors should be aware that differences between the US Generally Accepted Accounting Principles (US GAAP) and International Financial Reporting Standards (IFRS) accelerate in 2024 annual reports. CFA Institute continues its multi-decade fight for convergence undeterred.

Peak GAAP and IFRS Convergence Was in the Late 2010s

After signing a Memorandum of Understanding known as the Norwalk Agreement in 2002, the US Financial Accounting Standards Board (FASB) and the International Accounting Standard Board (IASB) embarked on a series of joint standard-setting projects to converge US GAAP with IFRS. Those efforts were successful in some areas. Standards on business combinations, segment reporting, consolidation, the fair value option for financial instruments, revenue recognition, and leases converged.

But things changed during the joint standard-setting projects on credit losses. Global finance ministers and regulators urged standard setters to work together on a converged standard that would improve shortcomings in credit loss recognition identified in the Global Financial Crisis. Yet different standards were issued: Current and Expected Credit Losses (by the FASB) and IFRS 9 and Financial Instruments (by the IASB).

GAAP and IFRS Differences in 2024 Annual Reports

After the split over the credit loss standard, the two standard setters each embarked on their own agendas and have issued several new major standards. The effective dates for these new, post-convergence standards are now approaching.

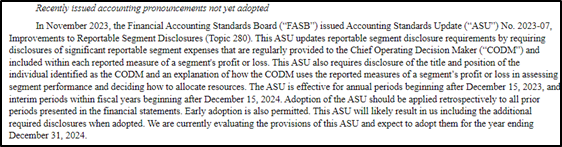

The first new major standard is the FASB’s Improvements to Reportable Segment Disclosures, which is effective in 2024 annual reports. Eagle-eyed readers of 10-Ks and 10-Qs filed since the end of last year will have noticed companies’ disclosures about this standard, like the following from Tesla Inc.’s 10-Q filed on July 24, 2024.

In short, the new segment standard requires companies to disclose more about expenses that are included in each of their reportable segments’ measure of profit and loss and to make certain segment disclosures on an interim rather than only annual basis. The new standard does not, however, change how companies identify their operating segments, aggregate those operating segments, or the quantitative thresholds used to determine reportable segments. We’ll have more to say on this new segment reporting standard in an upcoming series of blog posts on segment reporting. In the meantime, see our comment letter to the Exposure Draft last year.

Importantly, the IASB has not issued a similar new standard for segment reporting for IFRS nor does it have an ongoing standard-setting project on the topic. While we’ve yet to see how companies will implement the new standard, we generally expect segment disclosures by US GAAP reporters to become longer and more detailed than their IFRS-reporting counterparts.

Another major new standard in the post-convergence era is the IASB’s IFRS 18, Presentation of Financial Statements, which becomes effective 1 January 2027. IASB Board Member Nick Anderson’s Enterprising Investor blog post, “IFRS Accounting Standard Will Support Better Investment Decisions,” is a good primer on the IFRS 18 requirements:

- Operating, investing, and financing categories and operating profit and profit before financing and income taxes subtotals will need to be stated on the income statement.

- Certain non-IFRS performance measures will be brought into the notes to the financial statements and thus into the audit’s scope.

- More detailed guidance on the grouping, presentation, and disclosure of information will be expected in financial statements.

These requirements will be specific to IFRS because the FASB has not issued nor is it working on a similar standard for financial statement presentation under US GAAP. While we’ve yet to see how companies will implement the new standard, this may create a significant divergence with US GAAP, particularly the requirements to bring certain non-IFRS performance measures into the financial statements.

The segment and financial statement presentation standards are just two examples of standards in the post-convergence era. Several more are slated to become effective in 2025 and 2026, with more on the horizon that have been proposed in exposure drafts.

Table 1. Selection of upcoming standards in the post convergence era.

| US GAAP | Effective Date | IFRS | Effective Date |

| Improvements to Reportable Segment Disclosures | 2024 | IFRS 18, Presentation of Financial Statements | 2027 |

| Improvements to Income Tax Disclosures | 2025 | ||

| Accounting for and Disclosure of Crypto Assets | 2025 | ||

| Expected to be Issued: | Expected to be Issued: | ||

| Disaggregation – Income Statement Expenses | 2026 | Financial Instruments with Characteristics of Equity | TBD |

| Accounting for Software Costs | TBD | Business Combinations | TBD |

| Accounting for Environmental Credit Programs | TBD |

CFA Institute Continues to Fight for Convergence

CFA Institute has advocated for convergence in accounting standards for decades. When we last surveyed CFA Institute members on convergence, 91% of member respondents globally supported having all companies throughout the world use a single set of accounting standards to prepare general purpose financial statements. Members agreed that a single set of accounting standards enhances comparability between companies and reduces complexity in the analysis of companies.

We have an opportunity over the next couple of years to get convergence back on the standard setters’ agendas. The FASB is doing an agenda consultation this year after two years of active standard setting. The IASB is not. But, the IFRS Foundation has been spending considerable time and resources on sustainability standards and the new international sustainability standards board, which got off the ground in 2023, and may increase its attention to financial reporting standard setting. We intend to use this opportunity to vigorously advocate for convergence on behalf of investors.

For more information about our advocacy and to view responses to exposure drafts and standard-setting consultations, see CFA Institute Research and Policy Center’s Financial Reporting topic page.

I just read this blog, and it’s a fascinating look at the ongoing efforts to converge GAAP and IFRS. 📊 As someone running an accounting firm, I find this topic particularly relevant. The CFA Institute’s commitment to this convergence is encouraging, and the insights provided are really helpful for staying updated on these critical developments. Thanks for shedding light on this important issue!