Don’t Get Too Excited Just Yet

With prospects for GDP brightening, it would be an easy mistake to get caught up in the excitement of a return to economic normalcy by pursuing ever-increasing equity valuations. After all, if markets did well throughout the Great Recession, just think what lies ahead with GDP poised for a near-term bout of growth. The instinctual answer is obvious in that valuation expansion is on the way, but the math illustrates any such gains would likely be fleeting at best. So, don’t get too excited just yet about positive economic news, because there is little to be optimistic about if you consider the likely path of capital markets from here.

Admittedly, prevailing economic indicators are very positive in spite of such secular concerns as massive societal debt, out-of-control federal spending, and historically poor labor conditions. The auto industry continues to surge, real estate is increasingly strong, and with interest rates at historic lows, there is no reason to believe either sector will reverse course soon. Moreover, rising mortgage costs will ensure a big pop in real estate as people scramble to lock in low rates while they can. Rising home prices and expanding construction will boost household net worth, jobs, and consumer spending. So, it is likely we will continue to see positive economic news for the time being and valuation expansion as a result.

Nevertheless, you have to ask yourself what a good story is worth and how likely further valuation expansion is from here. GDP growth is nowhere near the peak conditions needed to push PE ratios materially higher, a result of unprecedented monetary policy over the last half decade and its distortive effects on long-term asset pricing.

We must keep in mind that the economy is not doing all that well on a real or per capita basis. It is just that conditions are improving from bad to possibly good, which has an extremely positive effect on investors. We are living through one of those textbook situations where people tend to overpay for good news, a behavior easily exacerbated by five years of economic malaise and nearly free money. It may seem hard to believe as we come out of a recession and the jobs market remains in ruins, but equity markets are expensive.

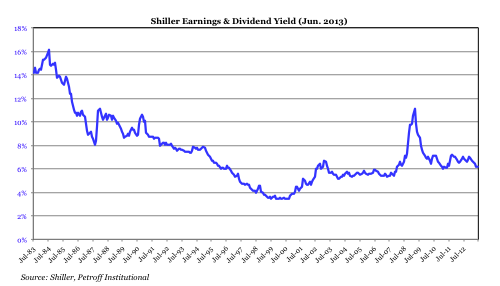

To understand this point of view, consider the chart below, which shows the Shiller Earnings and Dividend Yield (SEDY) for the S&P 500 over the last three decades. Currently, the SEDY adds up to around 6% and has been lower only during the tech and credit bubbles, which we all know worked out well for investors. This is hardly a situation where upside abounds for equities, which implies downside is significant. In this regard, downside applies not only to abrupt changes in valuations but also to the long-term failure to realize equity-like returns, a death knell for maintaining real portfolio spending power over time.

Still, near-term economic trends should provide ample room for upside so long as interest rates remain artificially low. We have seen evidence of this over the last few weeks as valuations rose even after the Fed’s warning that tightening is inevitably coming in one form or another.

We would argue, however, that valuations have become too expensive in the context of most institutions’ return goals and that now is the time to scale back rather than increase risk. Our point of view is best expressed by the concept of defining whether markets are offering a good deal as a function of required portfolio returns.

For example, if a portfolio’s return goal is 1%, equities trading at a PE ratio of 100 would present a perfectly fine long-term investment even without further upside potential. This is because a PE ratio of 100 would equate to an earnings yield of 1%, which, in addition to dividends, would provide a more-than-sufficient return. Alternatively, if a fund needs to earn 8%, equities at a PE ratio of 100 could not even be considered as a viable long-term asset, let alone one worth loading up on in hopes of capturing a little upside.

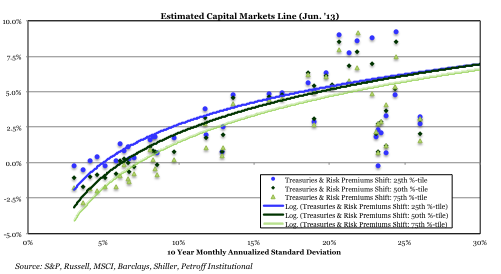

With this logic in mind and assuming that most institutional investors are trying to earn 6%–8% at the portfolio level, we believe it is fair to say that capital markets are broadly offering a bad deal to institutional investors. In the chart below, we estimate the global capital market line (CML) for assets ranging from cash to emerging-market equities. This analysis provides a simple visual interpretation of prospective market returns for a given amount of risk. These forecasts are based entirely on objective valuations and assume that interest rates and associated risk premiums return to various historical percentiles.

The smoothed lines in the chart represent the aggregate opportunity set for investors, which provides an easy reference tool for estimating portfolio returns. For portfolios holding equity allocations of 60%–80%, an aggregate standard deviation of 10%–15% is normal. On the basis of this assumption, it appears that diversified portfolio returns will earn between 3% and 4% over the next decade. The chart also indicates that riskier assets, such as equities, will earn little more than 5%.

So, the conclusion here is that the math of valuation-based forecasting shows that capital markets are expensive and prospective returns are uninspiring to long-term investors. The good news, of course, is that rates are headed higher and will shift the CML upward as a result.

Capitalizing on this opportunity is relatively simple. You just need the discipline and patience to reduce risk and wait for higher interest rates and cheaper valuations. Sometimes, walking away from a bad deal is the wisest course of action for an investor.

This is not market timing—it’s rational investing.

1. The earnings yield is the inverse of the PE ratio. For example, a PE ratio of 20 would equate to an earnings yield of 5%.

2. As defined by the monthly annualized standard deviation of returns.