The Challenges of Incentivising Long-Term Financing in Europe

Commissioner Barnier’s wide-ranging Green Paper on Long-Term Financing opened the discussions on EU initiatives for finding the most effective policy framework to support substantial levels of investment in key sectors of the European economy by increasing funding from outside the banking and public sector. The paper explored many different avenues to foster the supply of long-term financing to the European economy, to diversify financial intermediation, and to encourage investment in long-term assets. Whilst the paper was welcomed in almost all circles, many challenges exist in getting this much- talked-about, long-term financing framework to work in Europe. (Read CFA Institute response.)

A recently conducted pan-European CFA Institute members’ poll asked respondents for their views on this issue as well as any viable solutions that could be put forward to help overcome the hurdles and encourage economic recovery. The results point to several obstacles to overcome.

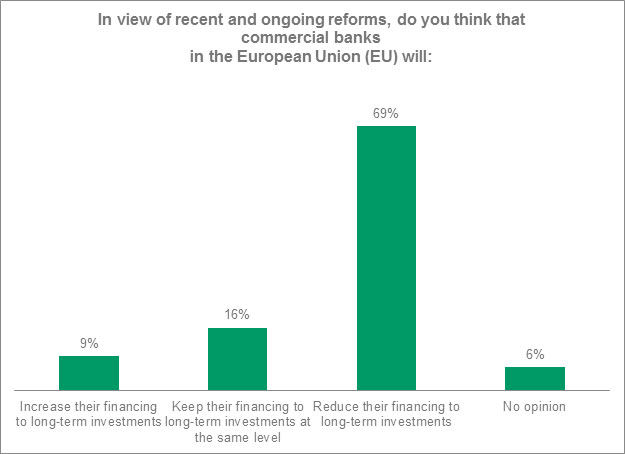

Source: CFA Institute

Firstly, and probably most importantly, whilst European banks have been deleveraging and trying to rebuild their balance sheets, often as a condition of government bailouts, bank lending to the real economy has dried up. This is critical for Europe, given that Europe’s corporates and households are much more dependent on bank financing (and less on capital markets) than in the United States or elsewhere. In our poll, 69% of respondents said they felt that commercial banks would reduce their financing to long-term investments in light of ongoing regulatory reforms.

Then there are industry concerns that CRD IV (legislation implementing Basel III) and Solvency II (legislation regulating prudential requirements for insurance companies) will reduce incentives to invest in long-term assets and (for banks) to lend to SMEs, as such activities incur higher capital charges. Sixty percent of respondents in our members’ poll stated that the new prudential rules for insurance companies (Solvency II) reduce initiatives to invest in long-term assets in favour of short-term assets.

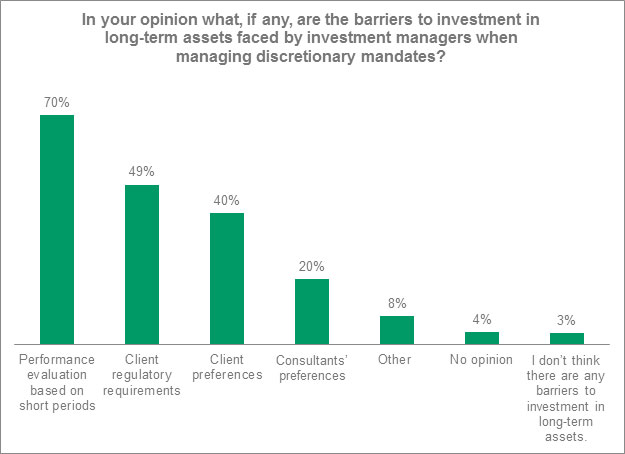

Seventy percent of CFA Institute European members responding to the survey believe that performance evaluation periods based on short time periods act as a barrier to investment in long-term assets. Furthermore 49% of survey respondents believe that client regulatory requirements act as another barrier to investment in long-term assets faced by investment managers when managing discretionary mandates.

Source: CFA Institute

Overall incentives towards short-termism should be removed by changes in criteria for institutional investment mandates (towards longer-term assets), and by a lengthening of performance evaluation periods for asset managers. Seventy-three percent of survey respondents believe that the current emphasis by institutional investors on short-term performance metrics should be discouraged. This would be the most important means of changing the attitudes of investment managers and their clients towards long-term investing.

Other key highlights from the CFA Institute member survey:

- In all, 62% of CFA Institute European members who responded to the survey support the introduction of a new category of EU Long-Term Investment Funds (LTIFs or ELTIFs). However, such a framework should be sufficiently flexible to allow for investments in different categories of assets (not just infrastructure), and investors’ liquidity requirements should be taken into account in the proposals, to make the framework attractive.

- The development of a European project bond market (52%) and a revival of securitization (44%) would be — according to CFA Institute European members surveyed — the most important factors to channel more long-term financing to the European economy. In particular, these options represent a promising channel for SME funding, with over 44% of survey respondents demonstrating support. However, progress towards a pan-European securitization market requires simple structures and better collateral transparency, as well as improvements in standardization of legal frameworks (bankruptcy laws, credit hierarchy, and guarantees, for example) which are currently very diverse at a national level.

- CFA Institute European members believe that enhanced corporate governance reporting could help promote long-term shareholder engagement. In particular, improving transparency of remuneration policies (64%) and enabling shareholders to have a non-binding vote on such policies (59%). A further 59% demonstrated support for strengthening the rules on voting transparency for institutional investors.

Although some of the initiatives discussed in the Green Paper have already been launched by the European Commission, much remains to be done. A broad approach to long-term financing is necessary, as no single initiative or funding source is going to be sufficient to inject adequate funds into the real economy. Investors’ needs, however, must be borne in mind when considering new public interest infrastructure products, as must the unintended consequences of the many recent regulatory changes and the ultimate cumulative impact on the real European economy.

Photo credit: ©iStockphoto.com/richterfoto