A Fuller View: Information to Assess Derivatives Credit-Risk Exposures in Banks

An invaluable source of information on bank-sectorwide derivatives risk exposures is the OCC Quarterly Report on Bank Derivatives Activities based on regulatory call reports. However, this report is focused on the US banking sector and there is no similar report covering non US-domiciled banks.

On top of reading industrywide reports, investors need to be able to monitor entity-specific exposures communicated through bank financial reports. That said, as reported in a 2013 CFA Institute publication, it can be challenging to readily discern the firm-specific aggregate derivatives exposures because of the often incomparable, incomplete, and fragmented disclosures within financial reports. In this piece, we place the spotlight on reported derivatives credit risk measures.

Offsetting Presentation and Disclosure, Differences across US GAAP and IFRS

Alongside collateral requirements, netting agreements between contracting counterparties are part of derivatives credit-risk mitigation measures. Concurrently, both US GAAP (generally accepted accounting practices) and International Financial Reporting Standards (IFRS) accounting requirements allow the offsetting (or netting) of derivatives assets and liabilities when these are presented on the balance sheet to better portray derivatives counterparty credit risk. A recent CFA Institute International Accounting Standards Board (IASB) joint video highlighted the updated and enhanced disclosure requirements related to the offsetting of derivatives assets and liabilities during their presentation on the balance sheet. (The requirements went into effect 1 January 2013.)

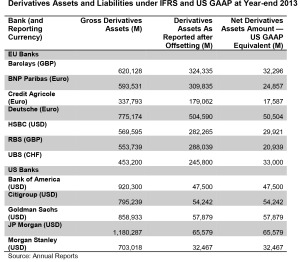

IFRS has more restrictive offsetting requirements than US GAAP. IFRS requires offsetting only when there is legal right and intention to settle simultaneously between the counterparties. US GAAP goes farther and allows the offsetting of all multilateral netting arrangements and cash collateral. As a result of differing offsetting requirements, reported derivatives assets under IFRS-reporting banks are of a higher magnitude than those under US GAAP, as illustrated below. For example, the gross derivatives assets of JPMorgan and other US banks are higher than those of EU banks, but the assets presented on balance sheet portray EU banks as having higher amounts of derivatives assets. Consequently, the balance sheet total assets reported under US GAAP and IFRS are not comparable.

That said, the updated IFRS and US GAAP offsetting disclosures make it possible for investors to make analytical adjustments to reported balance sheets so as to make them comparable. For example, as illustrated in the above table, the US GAAP equivalent of derivatives is reflected for EU banks based on information reported within the updated offsetting disclosures. Adjustments to derivatives assets and other offset financial assets to make them comparable will result in comparable total assets. In turn, this yields comparable accounting leverage (assets/equity) and other asset-based metrics such as return on assets across IFRS reporting and US banks.

More to Credit Risk Exposure than Offset Amounts

Even after being netted, the reported balance sheet derivatives assets (receivables) do not necessarily represent their maximum possible loss. Unlike the credit risk of loans and debt securities, which is unilateral (lending bank faces a one-way credit exposure from the borrower), credit-risk exposures of derivatives contracts (e.g., swaps) are usually bilateral. This means that each party to the contract may have a credit exposure to the other party at various points in time over the contract’s life (derivatives that are in the money today can be out of the money at a future date). Furthermore, because the credit exposure is a function of movements in market factors, there can be a potential future exposure not reflected in currently reported fair value. As an excerpt from the analysis in the 2014 OCC quarterly report, the table below shows the credit-risk exposure is a combination of the bilateral netted exposure and the potential future exposure (PFE). PFE is usually part of the risk-reporting section (e.g., Basel Pillar 3 information). To enhance financial analysis, there remains an opportunity to integrate financial statement disclosures (e.g., offsetting) and the related relevant risk reporting information (e.g., PFE).

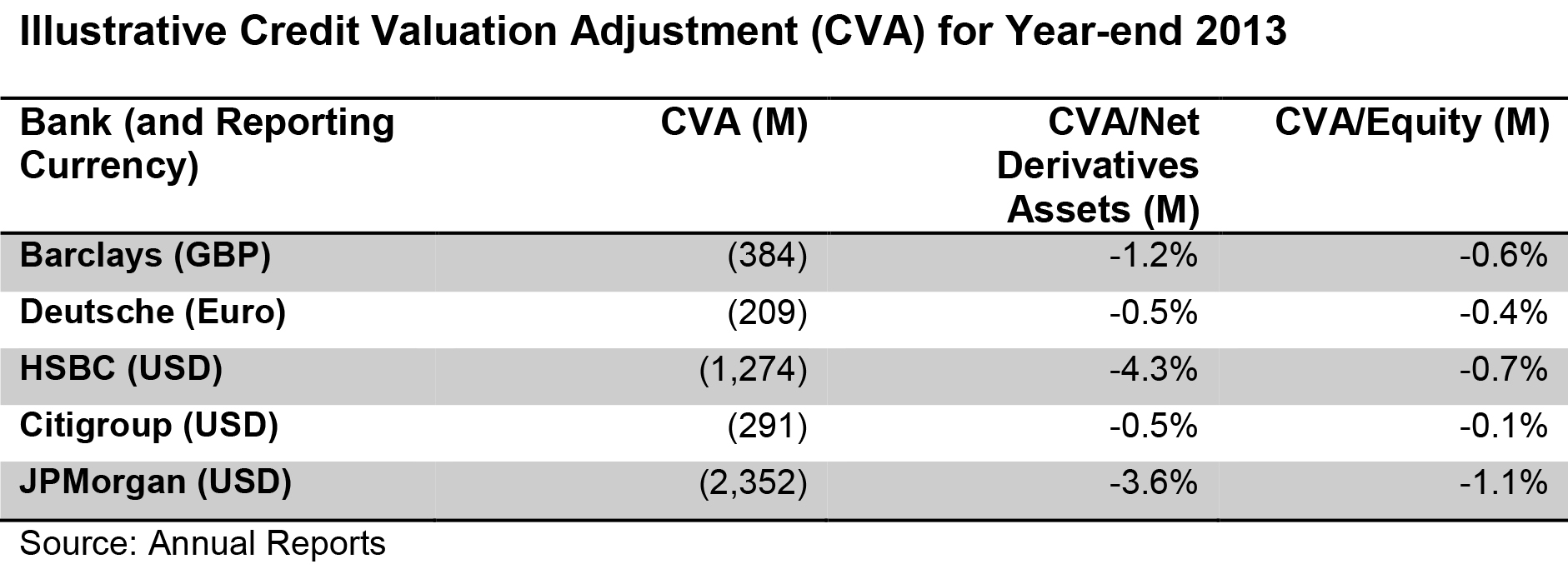

Another derivatives credit risk-related measure is the credit value adjustment (CVA). CVA is the adjustment made to the fair value amount of derivatives receivables due to the deterioration in credit quality of counterparties. CVA amounts can be material (e.g., JPMorgan and HSBC; see table below). The CVA is somewhat analogous to allowance for loan losses. That said, CVA is hard to compare across banks due to differences in how it is measured (see Ernst and Young’s recent publication highlighting CVA measurement challenges) and the lack of adequate disclosures on inputs and assumptions made in the CVA calculation.

In addition, unlike the relatively detailed reporting of loan credit risk, which includes allowance for loan losses alongside a profile of loan charge-offs and recoveries, similar details are scarcely provided for derivatives within general purpose financial statements, and this constrains the holistic assessment of derivatives credit risk. This latter information can help investors to discern how changes in macro-economic environment could impact derivatives-related write-offs (see Graphs 7 and 8 of the OCC June 2014 quarterly report).

In conclusion, this is a high-level view of some of the key derivatives credit risk measures and state of play of disclosures. The key message is that a multi-faceted view is required to judge derivatives credit-risk exposures, and yet the required information is not usually all in one place. In a future blog post I will examine the measures and disclosures related to the liquidity and market risk of derivatives.

If you liked this post, consider subscribing to Market Integrity Insights.

Image credit: Stephen Campbell, 2014

Great Insight!