Convexity Hedging: What Is It, and Why Does It Matter?

It only took a small backup in U.S. Treasury (UST) rates ― 10-year UST rates moved from 1.58% in early December to ~2.00% today ― for pundits to speculate on whether rates will drastically increase. Observant readers will have noted that various sell-side researchers and other market commentators have mentioned “convexity hedging” as something that could exacerbate a selloff in UST rates. Here I take a high-level look at what convexity hedging is and how it affects the UST market.

The asset class most affected by convexity hedging is agency mortgage-backed securities (MBS). These securities are common to such institutions as money managers, insurance companies, commercial banks, and hedge funds, among others. Since quantitative easing was put into place a few years ago, the Federal Reserve has become a large buyer of agency MBS and now owns just over $1 trillion of bonds. Although some participants do not need to hedge the interest rate risk of holding agency MBS, a large percentage of buyers do. The difficulty of hedging agency MBS lies in the fact that the bonds exhibit negative convexity.

That is, all else being equal, an increase in interest rates will lengthen the bond as prepayments slow down, but a decrease in interest rates will shorten the average life of the bond as homeowners refinance (prepay) into a lower rate. As one might imagine, as UST rates have fallen precipitously over the past few years, prepayments have accelerated on high-coupon mortgages. Bankrate.com shows the 30-year fixed average rate at 3.64% today, down from more than 5% in 2009.

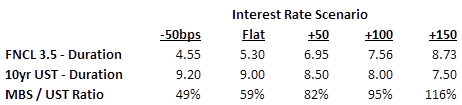

The implications of falling mortgage rates combined with the massive intervention by the Fed have created interesting dynamics in the MBS world. Naturally, with refinancing and new mortgage origination, the new, lower-coupon bonds have a lot more convexity. The following table shows the duration of a 30-year 3.5% mortgage pool under various interest rate moves.

As the table illustrates, the duration of the 30-year 3.5% pool rises from about 5.3% in a flat rate scenario to about 8.7% in a rate that is up 150 bps. One could debate the specific numbers, but it’s the general relationship that is most important to understand. If rates rise, the duration of the MBS bond rises as well. The amount of U.S. Treasuries needed to keep a given “hedge ratio” changes dramatically.

Yes, I’m thinking of the mortgage REITs that typically lever 30-year agency MBS 6–8×. How this relates to UST selling is obvious: If rates were to rise and MBS holders needed to adjust their hedge ratios, incremental UST selling would occur, potentially exacerbating a selloff. The effects would extend beyond U.S. Treasuries. Mortgage REITs can be forced sellers of mortgages if rates rise (prepayments slow) and prices fall enough. As shown in the table, duration could rise on a 30-year 3.5 from 5.3 to nearly 9. By mid-2012, mortgage REIT MBS outstanding surpassed $300 billion.

If you liked this post, don’t forget to subscribe to Inside Investing via Email or RSS.

Please note that the content of this site should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of CFA Institute.

Nice post. It shows how things could begin to cascade quickly.

It is really a nice and useful piece of info. I am glad that you

just shared this useful information with us. Please stay us up to date like

this. Thanks for sharing.

Looking at your post today, not only what you wrote easy to understand, but it foretold what had happened with rates in the last three weeks, especially the last week.

Thank you for sharing.

Useful post but shouldn’t the duration be measured in years and not percent?