COVID-19 May Permanently Quarantine Inflexible Leases

Real estate leases have long represented a point of disagreement between accountants and analysts (figure 1). This disagreement was the primary reason why the International Accounting Standards Board and Financial Accounting Standards Board went separate ways in finalizing lease accounting standards.

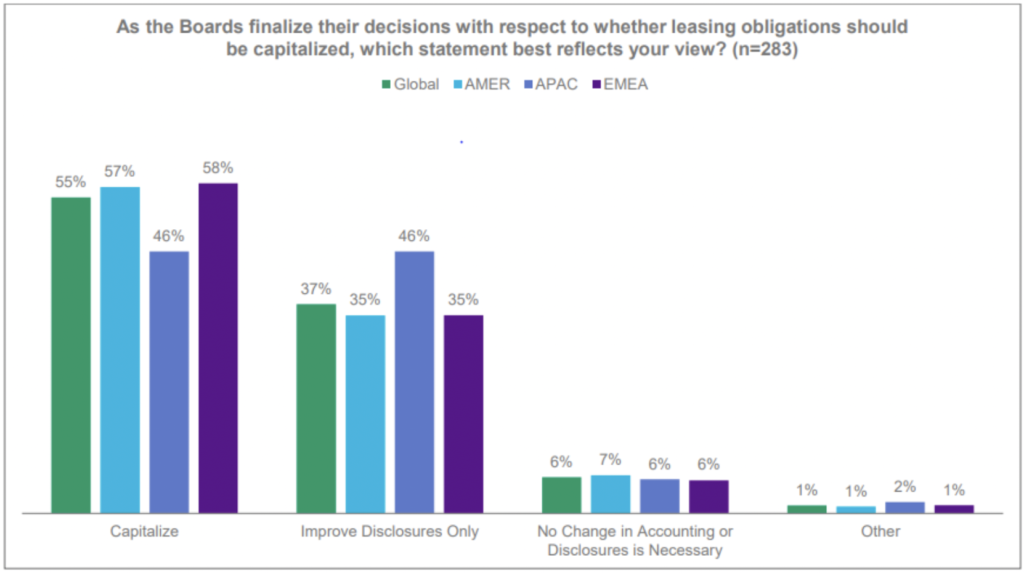

Figure 1. Lease Accounting Survey Report (October 2013)

Source: CFA Institute.

For a very long time, real estate leases remained off-balance sheet in accounting and on-balance sheet in investor analysis. The Investors’ argument is based on an economic assumption — that is, businesses operating on a going-concern basis need a real estate asset. A steady generational shift to the digital economy, however, has raised questions about the longevity of a bricks-and-mortar-only business. The coronavirus could further accelerate this shift.

Numerous bricks-and-mortar-only businesses may not survive the highly likely recession in 2020. And those that will survive will have no other choice but to move on a war footing to join the digital economy. Therefore, a post-coronavirus normalization will see lessees more determined to negotiate flexibility in lease contracts and overcapacity of commercial property could make landlords more willing to accept such demands.

Historical Perspective on Disagreement

Two prominent schools of thought consider real estate leases differently. A majority view such transactions as financing, whereas a minority view these leases as operating by nature. The only clause that makes such leases debt-like is the long-term contractual commitment. All other factors support these leases being treated as other fixed costs:

- Longer leases result in lower rentals whereas longer debt carries higher interest cost.

- Credit risk is reflected in tenant deposits (higher credit risk will require a higher deposit and vice versa) and not in rentals whereas credit risk is included in interest cost for debt contracts.

- Lessors prefer longer leases to generate stable cash flows and are willing to accept lower rents, whereas debt investors will never accept lower interest costs for longer contractual agreements.

Economically, real estate leases behave differently from debt obligations. Therefore, even in cases in which these are analytically adjusted as debt, these generally are referred to as “debt-like” obligations.

Analytically, the minority view was to treat such leases as operating leverage instead of financing leverage for the following reasons:

- simple and easier to analyze in comparison with financing leverage adjustments;

- arbitrary interest rate application to treat it as debt-like; and

- causing inconsistencies in credit analysis, such as a higher interest rate for speculative-grade issuers and a lower interest rate for an investment-grade issuer.

The standard setters’ main assumption (i.e., the majority view) is that a business operates on a going-concern basis and needs to have a real estate lease over a longer period. Therefore, real estate leases should be capitalized as a debt-like obligation. The reasoning was to treat such leases as financing for the following reasons:

- Comparability exists between issuers on an economic basis irrespective of whether the choice is to enter an operating lease, finance a lease or take a bank loan.

- A common analytical adjustment is to use a “multiple approach” to capitalize on operating leases. A commonly used “8 multiple” is based on a 6% interest rate and an average economic life of 30 years. This also addresses the previous criticism about simplicity and arbitrary interest rate application.

- The multiple approach ensures a consistent adjustment of financing leverage across industry sectors.

Online Disruption

The online disruption has turned the economic assumption upside down. A notable case study is Sears, which was founded in 1893 and was the dominant retailer in the United States. Its business idea of a mail catalog, known as the “Sears Wishbook,” became the foundation of its growth story. From the 1920s, Sears built its department stores and expanded outside its home country. From the 1950s to the 1970s, it expanded from suburban markets to malls. At its peak, it was selling everything from tools to houses. However, from the 1980s onward, Sears missed out on female consumers as an important demographic group, and new competition emerged from discount retailers (e.g., Walmart). The final hit came from online competition, and the group filed for insolvency on 15 October 2018.

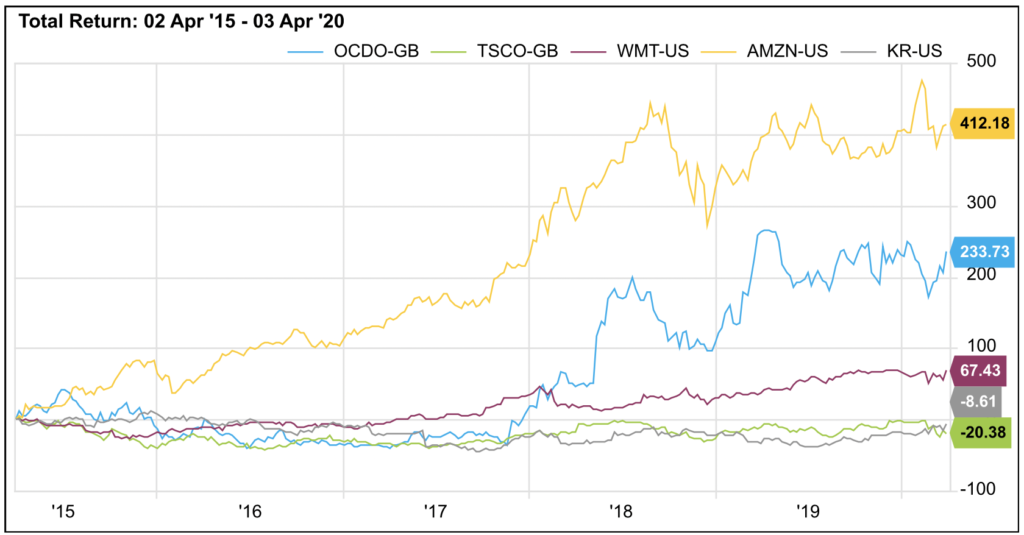

As one great business idea faded away, another replaced it. Ocado (a UK-based online grocery retailer) set up a business model based on its bet that online sales would rise as the tech-savvy younger population switched to purchasing groceries online. It made losses for a long time, but overnight, it became a key service provider to bricks-and-mortar retailers when Amazon announced its acquisition of bricks-and-mortar grocery chain Whole Foods in June 2016. The legacy retailers realized that the digital economy was no longer a niche market. Ocado’s total return (figure 2) over the past five years perfectly captures its story as legacy businesses started signing up deals to get a foothold in the digital economy.

Figure 2. Ocado’s Total Return (2015–2020)

Source: FactSet.

Cognitive Bias

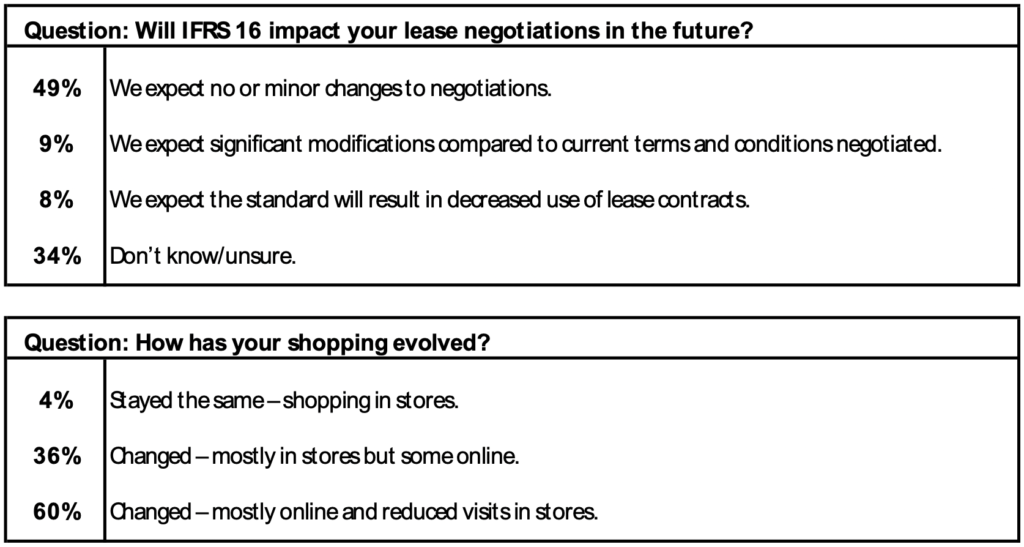

In a webinar hosted by Institute of Chartered Accountants of England and Wales (ICAEW), “IFRS 16 Leases — The Impact,” on 23 May 2019, 389 finance professionals were asked two questions to gauge their assessment of whether struggling bricks-and-mortar retailers facing increased online sales coupled with the new leasing standard[1] would see changes in future lease negotiations. The replies are given in figure 3:

Figure 3. Changes in Future Lease Negotiations

Source: ICAEW, CFA Institute (23 May 2019).

In response to the first question, around half of the participants expected no or minor changes in future lease negotiations. Only 17% expected that changing economics and accounting standards would result in either significant modifications or decreased use of leases contracts. Around one third were unsure at that point in time.

In response to the second question, 96% of the participants mentioned that their shopping habits had changed. A majority (60%) of the participants said they were doing most of their shopping online with reduced visits to physical stores. Only 4% mentioned that shopping habits had stayed the same as shopping in physical stores.

The combined results of these two questions could be explained with a cognitive bias. When things do not change for a long time, they are expected to remain the same. The survey responses confirmed the online shopping trend and confirmed the upcoming overcapacity problem for landlords.

An Intu Properties PLC press release on 4 March 2020 noted the status before the impact of COVID-19 outbreak:

The independent valuations of intu’s portfolio at 31 December 2019 delivered a valuation deficit of £2.0 billion for 2019, a like-for-like decrease in value of 22 percent for the year and around 33 percent from the peak valuation in December 2017. Weak sentiment rather than hard transactional evidence has been the key driver in the valuation deficit with net initial yield (topped-up) increasing by 95 basis points to 5.93 percent.

Post-COVID-19 Recovery

The recent COVID-19 lockdown has brought the global economy to a standstill. It has created new winners and losers. In the current crisis, players in the digital economy would come out as big winners.

According to a review of global retailers with combined revenue of around $5 trillion on FactSet, an annual rental cost of $136 billion was reported on 2018 financial statements. This amount accounts for about 2.7% of the combined turnover. The rental costs to turnover vary by the size of the retailer — for instance, for retailers earning less than $1 billion, the five-year average rental costs were around 5.9% of turnover. Therefore, if sales remain depressed in the post-COVID-19 recovery, the small retailers would be hit the hardest as the five-year average Earnings Before Interest and Tax (EBIT) margin was around 2.6%.

The lockdown, irrespective of how long it lasts, will:

- accelerate a shift to online shopping for consumers;

- force surviving retailers to aggressively pursue a shift to digital economy;

- make businesses rethink their commitment to renting office spaces when modern technology could be used to chip away at this fixed cost (this can reduce the carbon footprint and provide more flexibility for the workforce to work remotely, thus reducing commuting and flying); and

- make businesses renew their lease contracts with maximum flexibility and link to the variability of store sales to reduce overall leverage.

WeWork may have been a bad business model for an intermediary. This important technology solution, however, may address the overcapacity issue for landlords. Significant shifts in consumer habits, the aging population, and increased gig-economy workers are creating a secular trend that will become increasingly prominent with the passage of time. If this is the case, then the commercial rental income could become more volatile and cyclical in the future.

Conclusion

The majority view and the underlying economic assumption may be coming to an end. The minority view to treat real estate leases as operating leverage now has the technology and macroeconomic changes on its side. Only the post-COVID-19 recovery will reveal whether these changes will happen in the near term or over a longer period of time.

Regulators and standard setters should pay attention to these digital trends. Issuers should be required to disclose forward-looking business models to communicate management thinking about these issues. As technology-driven services replace unintelligent physical assets, these need to be captured both as an asset and as an obligation in accounting. Whether service obligation is an operating or financing leverage is a discussion for another day.

[1] IFRS 16 and US GAAP 842 Leases went into effect 1 January 2019. The new lease standards require real estate leases to be capitalized as debt on balance sheet.

Image Credit: © 2020 CFA Institute