Do Stock Screens Really Work?

Generating new investment ideas is a process that is usually glossed over and generally underemphasized in money management. But it is also an area investors take great pride in. Naturally, this pride leads to the formation of investment biases, which have adverse effects on this important first step of the investment process. For some reason, most people consider themselves exceptional stock pickers, no matter how poor their historical performances have been or how little they actually know about investing. In a more extreme example, a large portion of the middle-aged housewife population in South Korea spend the day at home trading online. Almost all of them consider themselves on par with the top fund managers because of their natural talent and superior market timing capabilities. In the United States, the usual “talking heads” in the media love to barrage us with self-gratifying commentary about their previous stock pick winners. But when they are put on the spot and asked what their next recommendation is, the typical response is to give a few extremely vague, hedged, and self-contradictory statements, which invoke such thoughts as, “So are you saying this is a buy or a short?” and “Can I slap you now?”

The reality is that there is no crystal ball that we can depend on to give a steady flow of investment ideas. The best we can do is to prioritize which companies to investigate further, followed by in-depth security analysis. But how can we prioritize when there are literally tens of thousands of companies to choose from? The most common methodology that fundamental investors use today is the stock screen. These screens use various input constraints to generate a narrowed list of companies that match certain criteria. For example, you could screen for all companies with a P/E of less than 10x, EPS growth rate of greater than 20%, and/or a market capitalization of greater than $1 billion. On the surface, the method seems fairly straightforward, quantitative, and unbiased. But it is important to first ask yourself how these input variables are selected in the first place. Investors generally tend to prefer companies that they are familiar with; even Warren Buffett recommends this approach. Let’s take yours truly as an example. Way back when, I used to work at Samsung, an Asian technology conglomerate best known for its mobile phones and memory chips. Over the years, I have developed an ingrained perception that the company is extremely well run, garners utmost loyalty among its employees, and overall seems like a great investment opportunity. The end result is that when I perform my next screen, I will subconsciously “manipulate” the input variables so that somehow Samsung pops up in my search for European health care companies.

Beyond the difficult task of selecting unbiased input constraints, the most serious problem with using screens arises from the actual data itself. For example, if you are screening for companies that have a minimum 20% expected future growth rate, the data the screen uses are based on forecasts that have already been predicted by sell-side analysts. The data are aggregated via services, such as Bloomberg or Thomson Reuters, which allow you to slice and dice according to your desired input constraints. By using this screen, you are assuming that these consensus estimates are indeed spot on. If you take a step back and think about it, your fundamental assumption is that consensus sell-side estimates are correct, so you have just convinced yourself out of your job as an investment analyst or portfolio manager. In actuality, these estimates can be either right or wrong, but it is your job to determine which one it is. The sample stock screen of a minimum 20% future growth rate could have produced a company that has more than 40% EPS growth and trades at an attractive 10x P/E multiple. But there is usually a reason why a stock would trade at such valuations because the consensus, or “market,” already knows this information and has factored it into the share price. You could have achieved equivalent share upside by finding a company with a 20% declining future growth rate trading at a 20x P/E multiple on consensus numbers.

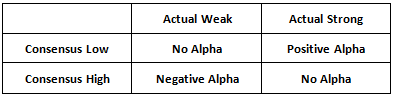

The purpose of actively investing in equities is to generate a positive return above what you could have earned simply by investing in the market, or alpha. Earning alpha is accomplished by capitalizing on situations in which the market has incorrectly predicted the outcome of events, not by generating a list of companies that the market already has high expectations for. The fact that the market already believes that a particular company is expected to grow 40% and trades at a 10x P/E multiple gives you no edge in generating excess returns over the market. The following figure generalizes the different outcomes achieved given low/high consensus expectations versus weak/strong actual results. As can be seen, it is difficult to generate positive alpha by screening for companies with strong consensus expectations.

How then do you identify opportunities that generate positive alpha while avoiding the pitfalls of investment bias? So far, we have discussed using stock screens to “pull” potential ideas through a contaminated filter (your biased input constraints) with the raw data ultimately being faulty itself (consensus estimates). What if instead of pulling investment ideas through a filter, we allowed them to be “pushed” to us, and all we needed to do was grab the right ones? In a perfect world, you would have an army of 100 investment analysts working for you, and you could theoretically have them analyze every liquid company that is scheduled to report earnings over the next few months. But because this luxury is probably not available to us ordinary people, a more practical solution to narrow down the pool of candidates is necessary.

The objective is to identify situations in which there is an asymmetry of information between market perception and reality. One method is to analyze companies that have had major corporate announcements, such as beating or missing earnings estimates, winning a significant order, or even going through an acquisition. The market’s level of misunderstanding and divergence of expectations generally tend to be greater surrounding these types of information events. One may argue that after these events are announced to the market, the information has already been calculated into the share price. This argument is theoretically true if you assume markets exhibit perfect efficiency. But if you assume semi-efficient markets, you can still capitalize on a certain portion of upside shortly after these news events take place. More importantly, these announcements tend to occur at inflection points in which companies undergo significant longer-term change. These inflection points generally coincide with a greater misunderstanding by the market and a larger set of information asymmetries. From that point, your security selection criteria — a separate discussion — should allow you to cherry pick your winners. At a minimum, you are starting your analysis with a company that is less likely to be fully understood by the market, and the selection process was not influenced by personal preferences, familiarity, or other investment biases.

Stock screens give the illusion of uncovering valuable insights that the market has yet to discover, when in actuality they are generating a list of companies that the market already has high expectations for. Push-oriented information screens allow you to quickly focus on only companies that are undergoing significant fundamental change, which coincides with a larger set of opportunities to generate alpha. Although this methodology does not come with a flashy securities worksheet or a software model, it does make an honest attempt to remove investment bias from the equation. The rest is up to you.

If you liked this post, don’t forget to subscribe to Inside Investing via Email or RSS.

Please note that the content of this site should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of CFA Institute.

Very true. Stock picking is an art. Screen can tell you one thing. Perhaps screen based on number of past historic durations with historic high/low multiple can refine. But, still the game is what is priced-in, already factored. Art is how to identify what has not been priced-in as Dan points out. Good flow of how good stock -pocker can not only identify what to invest, but when as well

Sam, thanks for the comment. Very true, your suggested refinements make a lot of sense. A comparison of current valuations relative to a given security’s own historical highs/lows would definitely add more insight to the analysis.

What about Greenblatt’s “Magic Formula” and some of the screens discussed in Quantitative Value?

I wouldn’t dismiss screening per se; I think it’s a matter of using the right metrics. I agree that screening with criteria based on forward estimates (such as P/EG) won’t get you too far, but with the right metrics (based on historic rather than forecasted data) I think you can find some good, undervalued companies.

There’s also a difference between using a screen as the sole method for picking stocks or using it as a starting point for equities that merit further research. I think the latter approach combines the “art” and “science” aspect of investing, and is certainly better than blindly choosing stocks just because they have a low P/E or P/B ratio, for example.

Elliot, thanks for the comment. You bring up a good point that I was actually going to mention in the original article, but avoided this time as I thought the reader might already be exhausted by the length! Screens based on historical data definitely deserve more merit as they avoid the consensus expectations obstacle. I also generally agree that screens can be a useful tool, as long as the user takes a step back and truly understands the data that is being analyzed and the inputs are chosen in an unbiased manner.

One of the underlying messages from the article is that a screen (whether traditional or non-traditional) is only the first step in the investment process. It is essentially a time management tool that allows the user to narrow the list of investment candidates to analyze further, not a blind tool that determines the final investment decision. What comes after this step is the “art” or personal investment criteria that must be applied as the second half of the investment process. I agree that investing must always have an art component integrated into the process, with “science” as the primary driving force that facilitates time management.