Do Dividends Create Shareholder Value?

I’ve recently had the pleasure of catching up with the Berkshire Hathaway Annual Report for 2012, which contains an interesting discussion on dividend policy. With dividends being all the rage in our low interest rate environment, this seems like a timely topic. Berkshire has famously never paid a dividend, yet Warren Buffett frequently extols the dividends Berkshire receives from its subsidiaries and publicly traded investments — from such companies as American Express, Coca-Cola, and IBM. This presents a bit of a paradox: Why are dividends right for American Express but not for Berkshire? Is Buffett being hypocritical?

The issue of when and how a successful company should return capital to shareholders — whether in the form of dividends or share buybacks — is far from simple, even for experienced investors and managers. A friend of mine who runs a thriving corporate governance watchdog group once challenged me on whether share buybacks are really very shareholder friendly. To the extent that share buybacks generate incremental value for ongoing shareholders, they do so at the expense of exiting shareholders (i.e., those whose shares the company buys back). Perhaps dividends are more equitable?

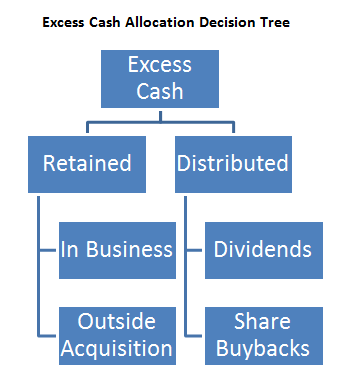

Buffett sets up the dividend policy discussion as a series of alternate uses for excess cash generated in a business. Here are the options:

At a high level, excess cash can either be retained or distributed to shareholders. If it is retained, it can either be invested in existing businesses (i.e., to “widen the moat” [competitive advantage], to expand, or to acquire a new business). If excess cash is distributed to shareholders, it can take the form of dividends or share buybacks. Each of these four options will provide some long-term return on the excess cash. Theoretically, we should evaluate these returns and select the option that will provide the highest one.

Much has been written on the left side of the decision tree, including Buffett’s criteria for selecting investments and his focus on return on capital. Less has been written on the right side: If a company decides to return capital to shareholders, should it pay dividends or buy back shares?

In the case of share buybacks, the key variable is the price of the stock relative to its value. Return on excess cash will clearly be higher for stock buybacks if a company has an opportunity to buy back its shares at a discount. The greater the gap between the price of the shares and their value, the higher the return on share buybacks would be. Additionally, company management should be in the best position to assess the value of the shares because managers have more and earlier access to internal company information than the market does. Unfortunately, the times when a company generates the most excess cash rarely coincide with the times when its stock trades at the greatest discount. In other words, when times are good, discounts are few and far between. If share buybacks are done at a premium instead of a discount (i.e., where the share price exceeds its intrinsic value), the share buyback will destroy value rather than create it. What should the company do if its stock is fairly priced?

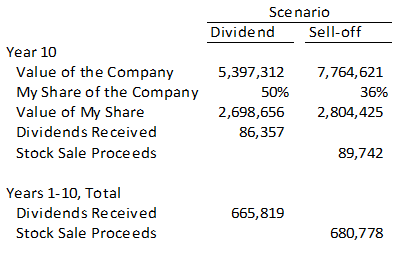

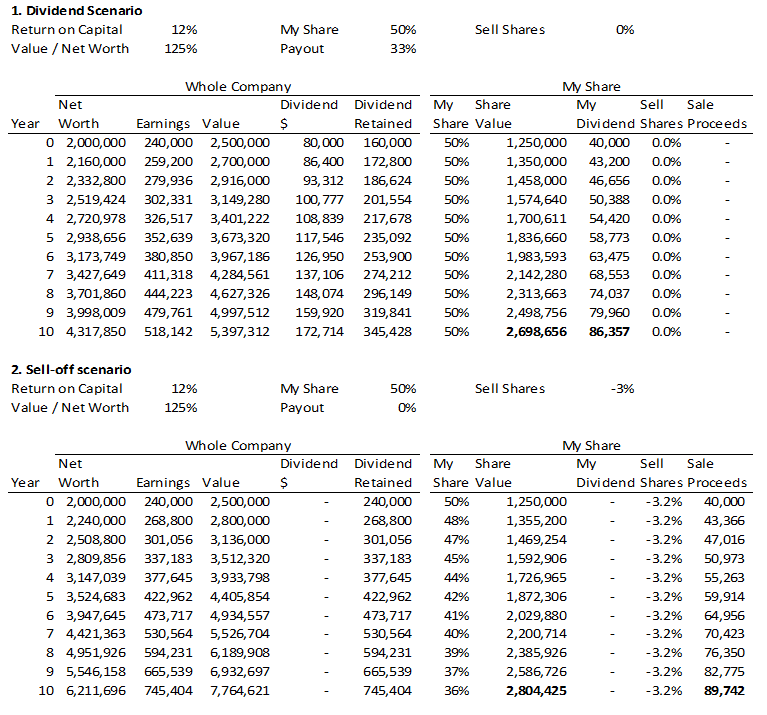

Buffett sets up a hypothetical company to answer this question: The company has a tangible net worth (book value) of $2 million. It earns 12% per year on this tangible net worth, so its earnings in the first year are $240,000. The company has two equal (50%) equity partners. Additionally, the company’s shares trade on a market, where buyers are always willing to buy or sell them at 125% of tangible net. In other words, the company’s price-to-book ratio is 1.25. The company goes through two capital distribution scenarios. In the first scenario, called “dividends,” the company distributes one-third of its earnings as dividends each year and retains the rest. In the second scenario, called “sell-off,” the company retains all of its earnings and one of the shareholders sells 3.2% of his shares each year in lieu of receiving dividends. Here is how these scenarios stack up from that shareholder’s perspective after 10 years (more detailed models are provided below):

In the dividend scenario, the value of the company compounds at 8% per year (12% return minus a 4% dividend). In the sell-off scenario, it compounds at 12% because no dividends are paid out. After 10 years, the sell-off scenario produces a more valuable company, but because the shareholder sells 3.2% of his shares each year, he owns less of it (36% versus 50% in the dividend scenario). These two factors partially offset each other, but the faster compounding of the company wins out and the shareholder ends up with a slightly more valuable stake in the sell-off scenario ($2.8 million versus $2.7 million).

In addition, the sell-off scenario gives the shareholder greater cash flows in the 10th year ($89,742 versus $86,357) and throughout the holding period ($680,778 versus $665,819). Thus, the sell-off scenario is superior at generating value to the dividend scenario in this case.

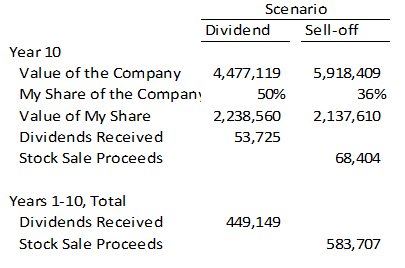

These numbers work out in favor of the sell-off scenario because of two key assumptions: First, that the company is able to compound its book value at 12% per year. Second, that the market will value it at 125% of its book value. The latter seems particularly reasonable for Berkshire, whose economic value certainly exceeds its book value, because of the massive and high-quality float generated by its insurance operations, among other reasons. The former assumption is more of a challenge. Although many companies have generated returns in excess of 12% per year for long periods of time, most have not. Berkshire certainly has in the past, but will it in the future? If the return assumption drops from 12% to 9%, it is harder to choose the right policy: The dividend scenario provides a more valuable stake at the end of the 10-year period but lower interim cash flows:

Ultimately, the retain versus distribute decision should depend on internal versus external returns (i.e., what returns the business could expect to earn internally versus what returns investors can expect to earn outside the business). In my view, our low interest rate environment coupled with a fairly to fully valued equity market means equity returns moving forward should be lower than they were in past few years, thereby lowering the bar for retaining capital for internal projects. Against this backdrop, a dividend is really an admission by management that they cannot find projects that would compound value at anywhere near 9% per year, as in the previous model.

Here are the full 10-year models:

Dear Alon,

I found your article very interesting, but I am a bit confused with your findings. My understanding is that “sell-off” is not directly comparable to buybacks or dividends, because it does not affect the cash balance of the company.

I have learnt that in the theoretical Modigliani-Miller framework investors are indifferent between dividends and buybacks. The effect of buybacks is also independent from the tender price. Suppose that the offer price is over fair value. Then every shareholder should tender his stocks. If stocks are repurchased proportionally, there is no transfer of value, because the premium paid is distributed among shareholders proportionally to their holdings. Therefore in theory the management cannot create value for shareholders via share buybacks. Naturally, this is just a theory and you probably cannot expect that all investors behave rationally.

I believe that the major difference between dividends and buybacks comes from the tax treatment – differences in capital gain tax and dividend tax rates.

What do you think? I would really appreciate your comments on it.

Best regards,

Jakub

Dear Jakub Kolodziej,

I see your question about why the author differentiated between shares buybacks and dividends. Here is my opinion:

I also have learnt that buybacks and dividends are the same. But when i read carefully, i find that the indifference they have mentioned is just the wealth of a shareholder at that year. When you receive dividends from the company, your money can’t earn profit itself, not like the case the company remains your money and make profit from this (ROE).

Example: in 2002, no matter how you choose buybacks or dividends, your wealth is the same. But from 2000 to 2005, there is the difference on your wealth when you choose buybacks or dividends.

Maybe my explanation isn’t clearly enough. I hope i will receive some complements about this subject!

Best regard,

The problem with this theory is that while the choices may start out that way,the need to maintain and increase a dividend can easily become a millstone around a company’s neck when good times turn to bad – as a means of trying to support the share price.

Paying and increasing a dividend is the last thing a company should do – after all productive self-investment and paying back all debt.

Very good piece.

This is a good framework to employ when thinking about Buffett / Munger’s strategy of compounding “winners” over time. I.e. investing in company’s that produce returns that are in excess of their cost of capital over the long run, on the basis of a sustainable competitive advantage or “moat” to enable compounding, and buying such companies at a “fair” price or, when Mr. Market affords the opportunity, at a discount to estimated intrinsic value.

This is a piece of the jigsaw which shows the power of compounding. A potential third analysis above could be a “no dividend / no sell-off” scenario, where all the profits are reinvested at the same rate of ROE (i.e. return on incremental invested capital is equivalent to that of the historical profile – difficult to achieve without a moat), which would show even greater returns (especially if taxes are taken into account in the three scenarios) of compounding at a high ROE.

There are some interesting fundamental multiples which are not widely used, the inputs for which include ROE, ke, % of incremental invested capital which returns excess returns (i.e. “70%” would achieve the 12% ROE in your example, while the remaining 30% would achieve Ke) and the time (in years) of that outperformance (driven by how strong the competitve advanatge is maintained). It’s an interesting may of highlighting the power of compounding high ROE/ROIC businesses with moats.

Best regards