Why Loan Growth is Important and What it Says about Inflation and Interest Rates

Investment professionals say over and over that this economic recovery is different, and with good reason. Gone are the days where the leveraging of consumer balance sheets is a primary economic growth driver. As most are well aware, during this recovery the Federal Reserve has taken unprecedented monetary policy actions in an attempt to jump start the economy. But how important are the actions taken by the Fed when contrasted with the activity of the banking system as a whole?

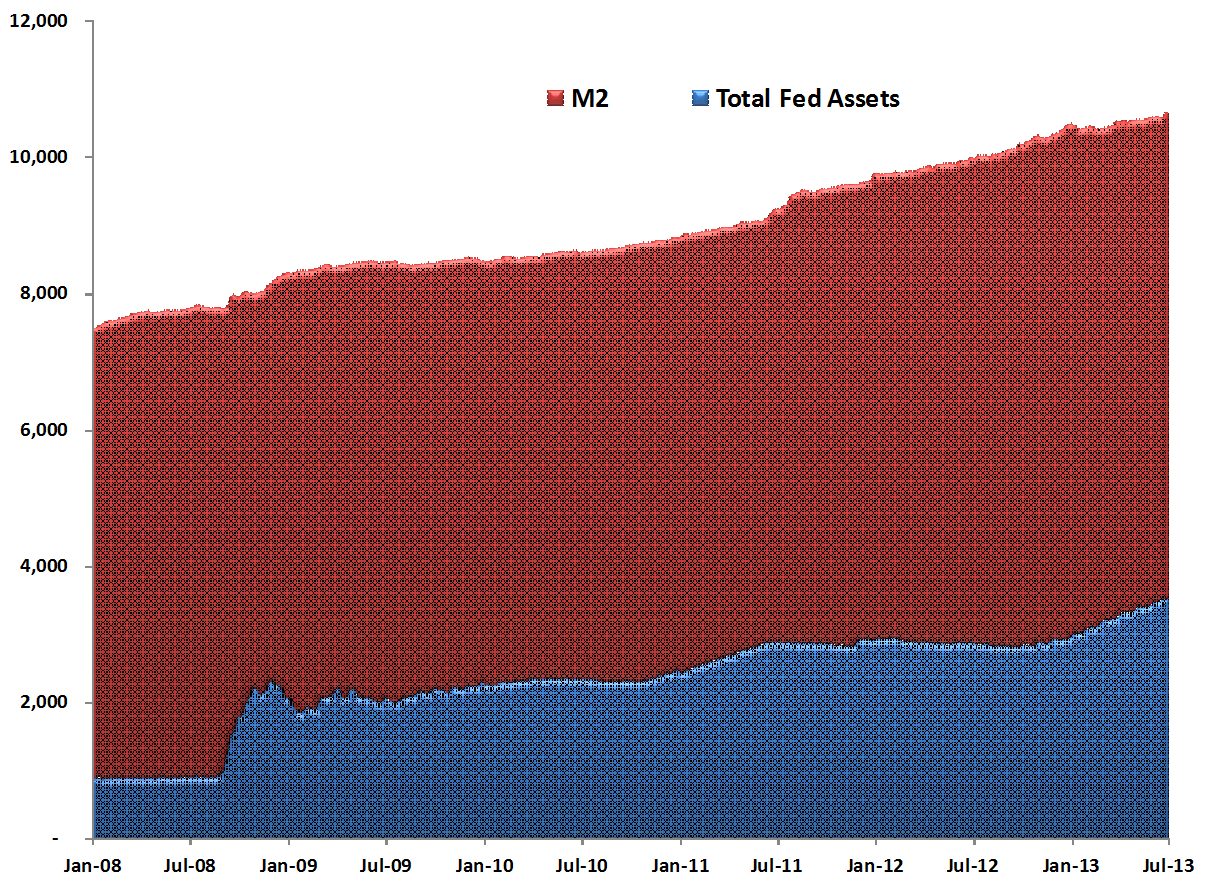

The Monetary Base is a Small Percentage of Broader Measures of Money Supply

The chart below shows the Fed’s total assets as well as a broader measure of the money supply called M2. The Fed’s balance sheet has grown from roughly $900 billion at the beginning of 2008 to nearly $3.5 trillion today. Skeptics cried that the Fed was “printing money” which would ultimately lead to wild inflation. Despite a $2.6 trillion increase in the Fed’s balance sheet (which increases the monetary base), as we can see below it is actually a very small percentage of broader measures of money supply such as M2 which incorporate credit creation from bank lending.

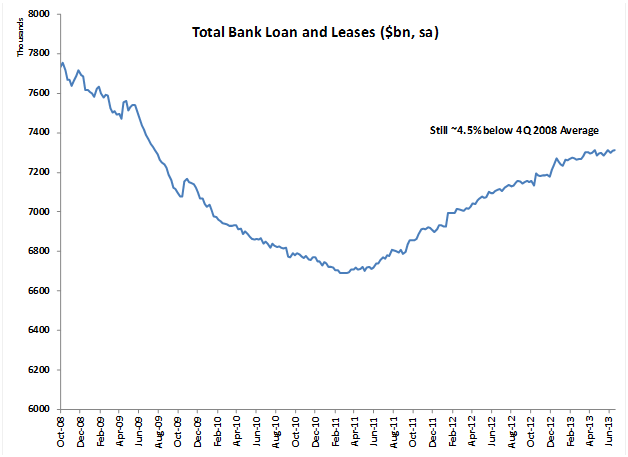

Bank Lending Activity Provides Clues to Increases in Broad Money Supply

Instead of focusing on how big the Fed’s balance sheet is, investors should instead be watching loan growth at commercial banks. The majority of the growth in broader money supply is going to come from credit creation via new loans made by banks. The chart below shows that while total bank loans and leases have increased from a trough in mid 2011, we are still roughly 4.5% below the 4Q 2008 average.

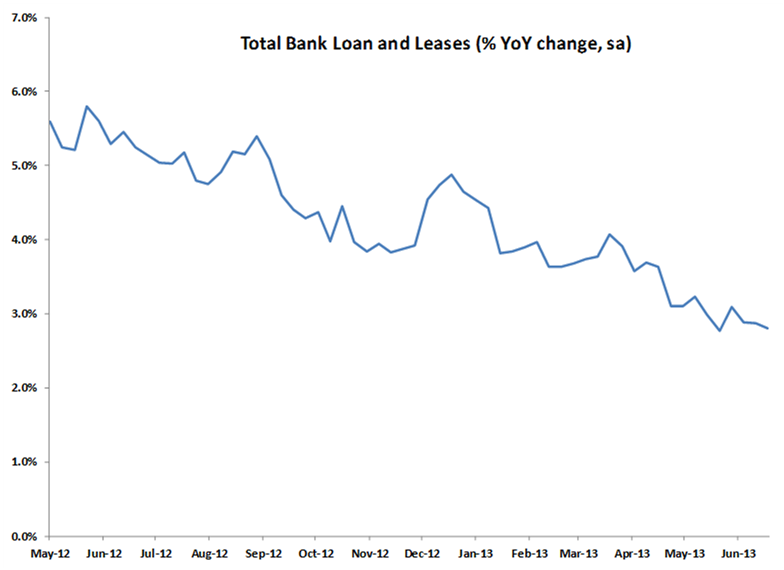

The nearer term trends are less encouraging. On a year over year basis total loans and leases are growing at a decreasing pace. In May 2012, loans and leases were growing at a YoY pace of almost 6%, while today that rate is under 3%.

QE’s Role in Bank Lending

To simplify, banks have two primary types of assets: loans and securities. Banks generally prefer to make loans as that’s their primary business, however excess liquidity is invested into securities such as USTs, Agency MBS, etc. In my opinion one of the primary goals of the Fed’s QE program was to encourage banks to lend by making the yields on investments unattractive.

Recent Rate Rise Could Pressure Loan Yields & Growth

The chart below shows the 30yr current coupon MBS yield on top, and the average loan rate on a C&I (Commercial and Industrial) loan on the bottom. I’m using the 30yr current coupon MBS yield as a proxy for what yield a bank could get if they invested in such a bond. These two rates have tracked very closely, with the loan rates on C&I loans generally a bit higher than the MBS rate.

With current coupon MBS yields jumping about a hundred basis points, or one percent to 3.39% as of July 18th, will banks continue to make sub 3% loans when they could buy a government bond at 3.39%? It is reasonable to conclude that lending rates (at least in that segment) may find some upward pressure.

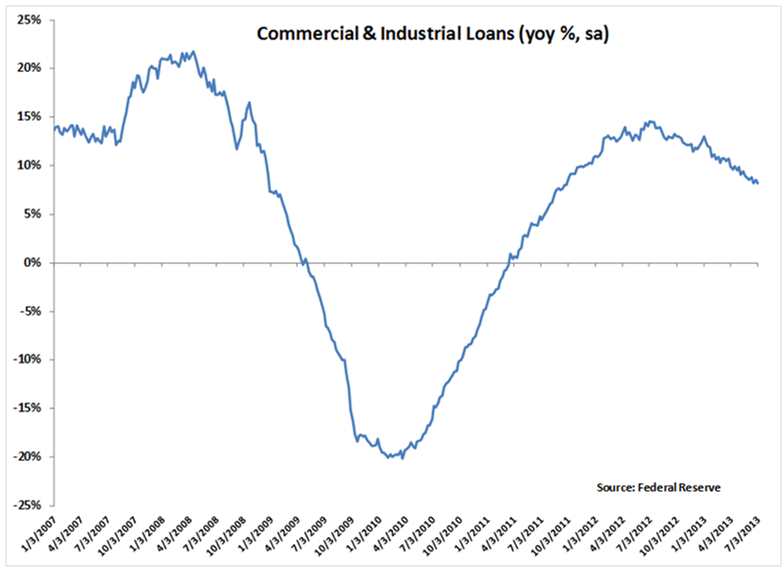

The next chart shows the year over year loan growth in the hot C&I sector. Banks have tried to diversify their loan books away from real estate given the recent credit crisis and have focused their attention on C&I loans. With the recent rise in rates the days of banks making 10 year amortizing C&I loans at 3% are likely over. Further, it wouldn’t be surprising to see further deceleration in C&I loan growth.

Constraints on Loan Growth, and Impact on Inflation & Interest Rates

Bank lending growth is an important driver of both interest rates and inflation. As broader measures of money supply are most impacted by lending and not the Fed’s balance sheet, it would seem unlikely that we could see a large jump in inflation without strong bank loan growth. This is also very relevant for interest rates since bank lending drives economic growth and inflation levels, both critical things for if/when we see the Fed raise the Fed Funds rate in the future.

At this point in time, I believe the greatest hindrance to further loan growth is demand driven rather than a supply issue such as credit standards. Banks offering sub 3% 10 year C&I loans are not the sign of a banking industry that’s averse to making new loans. Should we see a material pickup in lending, at the margin I would expect the see a follow through in higher rates and inflation.

While it’s not be all, end all, investors and analysts would be wise to pay close attention to trends in bank lending, as historically it has been a critical driver of key macro factors such as interest rates and inflation. Historically during times of large interest rate rises and/or inflation we’ve seen substantially higher loan growth than we’re seeing today.

If you liked this post, don’t forget to subscribe to Inside Investing via Email or RSS.

Please note that the content of this site should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of CFA Institute.

One comment on “Why Loan Growth is Important and What it Says about Inflation and Interest Rates”