Poll Results from the 24th Annual GIPS® Standards Virtual Conference

At the 24th Annual GIPS® Standards Virtual Conference, we conducted several polls about compliance, or planned compliance, with the 2020 edition of the GIPS Investment Performance Standards (GIPS®). Here’s what we learned.

Compliance with the 2020 Edition of the GIPS Standards

The effective date for the 2020 edition of the GIPS standards is 1 January 2020. GIPS Composite Reports and GIPS Pooled Fund Reports that include performance for periods ending on or after 31 December 2020 must be prepared in accordance with the 2020 edition of the GIPS standards. A firm may early adopt the 2020 edition after it meets all applicable requirements, but this is optional.

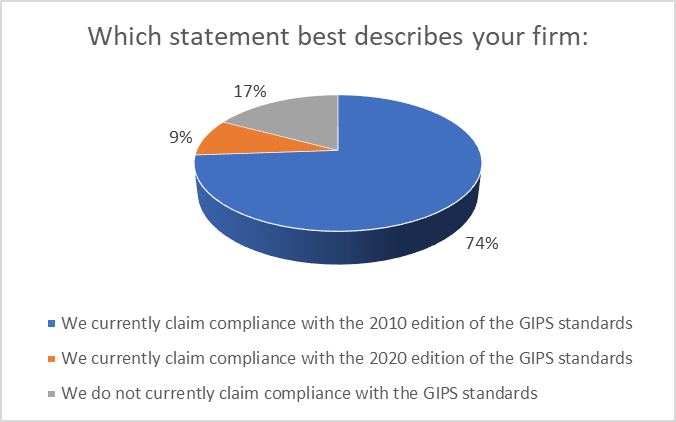

We asked firms if they comply with the 2010 edition, the 2020 edition, or neither. The majority of firms (74%) still claim compliance with the 2010 new edition, and only 9% of firms have early adopted the 2020 edition (figure 1).

If we remove from the poll those firms that do not claim compliance, 89% of the firms that currently claim compliance still comply with the 2010 edition of the GIPS standards and 11% have early adopted the 2020 edition of the GIPS standards (figure 2).

As a reminder, until a firm meets all applicable requirements of the 2020 edition on a firm-wide basis, it must continue to comply with the requirements of the 2010 edition. A firm that has not yet transitioned to the 2020 edition will continue to provide compliant presentations prepared in accordance with the 2010 edition to prospective clients until it includes performance for periods ending on or after 31 December 2020. At that point, the firm must comply with the 2020 edition of the GIPS standards.

Types of Portfolios Managed by Firms

The 2010 edition of the GIPS standards were based primarily on the use of composites, with a focus on presenting composite strategies to prospective clients. Before the 2020 edition, some firms that primarily manage pooled funds would state that the GIPS standards were not applicable to them. The 2020 edition of the GIPS standards are not as composite-centric and thus better accommodate the needs of managers of pooled funds, because it allows for the presentation of pooled fund–specific performance.

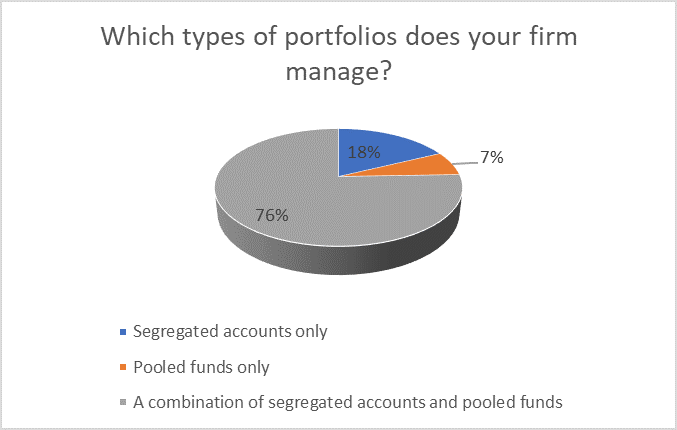

In this poll, we asked firms which types of portfolios they managed. The majority of firms (76%) manage both segregated accounts and pooled funds, whereas 18% manage only segregated accounts and the remaining 7% manage only pooled funds (figure 3).

Terminating Composites That Include Only Pooled Funds

Under the 2010 edition of the GIPS standards, firms were required to include all actual, fee-paying, discretionary portfolios in at least one composite, and this included pooled funds. Under the 2020 edition, firms need to create composites only for those strategies that are managed for or offered as a segregated account. If a pooled fund has a strategy that is not offered as a segregated account, the firm is not required to create a composite for that fund. When a firm adopts the 2020 edition of the GIPS standards, the firm may terminate any composite that includes only one or more pooled funds whose strategy is not offered as a segregated account. A firm that wishes to continue to maintain composites that include only one or more pooled funds is welcome to do so. Many firms are choosing to do this because they want to have a composite available if they subsequently decide to offer the strategy of a pooled fund as a segregated account.

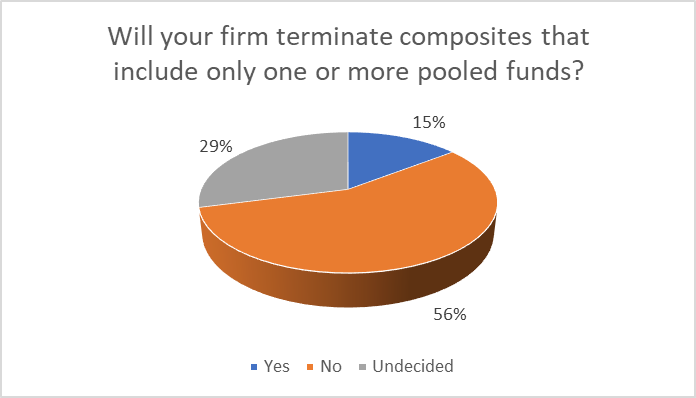

We asked firms if they intend to terminate composites that include only pooled funds. Considering only those firms that have such composites, 15% of firms indicated that they plan to terminate their composites that include only pooled funds. The majority of firms (56%) will not terminate these composites and 29% are undecided (figure 4). This is to be expected because many firms have already built these composites and see no reason to terminate them. We expect that firms that attain compliance in the future may choose not to create composites that include only pooled funds.

GIPS Reports for Limited Distribution Pooled Fund Prospects

The 2020 edition of the GIPS standards has two types of pooled funds — broad distribution and limited distribution — and they have very different requirements.

A broad distribution pooled fund is a pooled fund that is regulated under a framework that would permit the general public to purchase or hold the pooled fund’s shares and it is not exclusively offered in one-on-one presentations.

A limited distribution pooled fund is any pooled fund that is not a broad distribution pooled fund.

Firms are required to make every reasonable effort to provide a GIPS Report to prospective investors for limited distribution pooled funds. Firms have no obligation, however, to provide a GIPS Report to prospective investors for broad distribution pooled funds. Firms may provide a GIPS Report to prospects for broad distribution pooled funds, but this is optional.

The GIPS Report provided to prospective investors for a limited distribution pooled fund may be a GIPS Pooled Fund Report for the respective pooled fund, or it may be a GIPS Composite Report if the pooled fund is included in the respective composite.

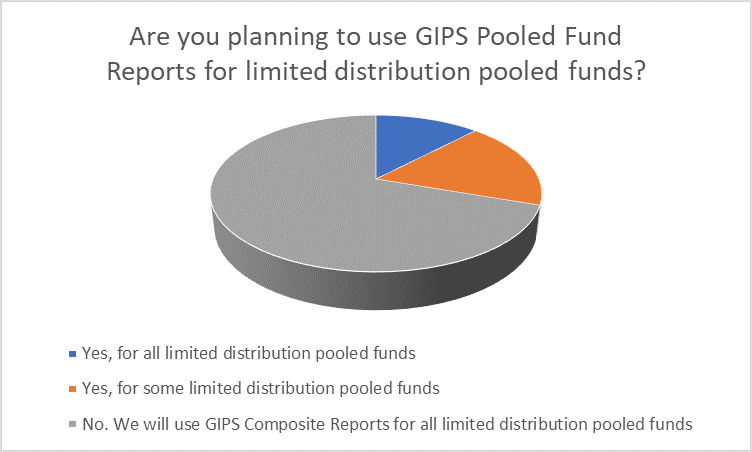

We asked firms which type of GIPS Report they expect to provide to prospective investors for limited distribution pooled firms. For those firms that manage limited distribution pooled funds, the majority (70%) of the firms surveyed plan to provide GIPS Composite Reports and not GIPS Pooled Fund Reports. This is not surprising because many firms currently follow this procedure. Approximately one-third of the firms will take advantage of the new option to provide a fund-specific GIPS Pooled Fund Report for all (12%) or some (18%) of their limited distribution pooled funds (figure 5).

We expect that firms newly claiming compliance with the GIPS standards will be more likely to use GIPS Pooled Fund Reports versus firms that currently claim compliance and already have procedures in place for distributing composite reports.

Carve-Outs with Allocated Cash

A carve-out is a portion of a portfolio that is by itself representative of a distinct investment strategy. For example, a firm may wish to carve out the performance of the equity segment of balanced accounts. A firm may include carve-outs in composites only if the carve-out includes cash and any related income.

Before the 2010 edition of the GIPS standards, firms were allowed to allocate cash to carve-outs. Under the 2010 edition of the GIPS standards, firms were no longer allowed to allocate cash to carve-outs. Instead, to be included in a composite, a carve-out had to have its own cash. Given the difficulty with establishing separate cash accounts for multiple carve-outs, many firms were forced to stop using carve-outs. Additionally, carve-outs are widely used by private wealth managers and mangers of private market investments. For these reasons, it was ultimately decided to once again allow firms to allocate cash to carve-outs. Firms complying with the 2020 edition of the GIPS standards may include carve-outs with allocated cash in composites and may do so for all periods.

In this poll, we asked firms if they are planning to create carve-out returns with allocated cash. The majority of firms (70%) do not plan to utilize carve-outs with allocated cash. Many of these managers may already have carve-outs managed with their own cash, so they do not need to allocate cash. Some firms (9%) do plan to use carve-outs with allocated cash, while the remaining 20% are undecided (figure 6).

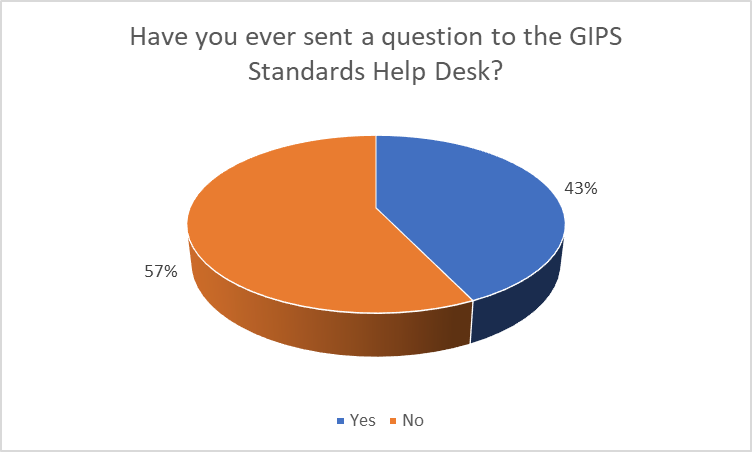

GIPS Standards Help Desk

The Global Industry Standards team at CFA Institute was curious to see what percentage of conference attendees have sent questions to the GIPS Standards Help Desk. Although we see these questions first-hand, we cannot tell what percentage of organizations are using the Help Desk as a resource. The results were split almost down the middle: slightly less than half of the respondents (43%) have sent a question to the Help Desk and 57% of respondents have not (figure 7).

Conclusion

A goal of the 2020 edition of the GIPS standards was to be relevant and applicable to all asset managers, including managers of pooled funds and alternative investment strategies. We also wanted to make transitioning to the 2020 edition as straightforward as possible for firms that already complied with the 2010 edition. We therefore provided more flexibility for presenting performance of specific funds to prospects and using carve-outs. On the basis of the results of these polls, we see that firms are taking advantage of the new options provided in the 2020 edition of the GIPS standards.

Photo Credit @ Getty Images / Klaus Vedfelt

The survey shows 2020 edition is not yet on track…