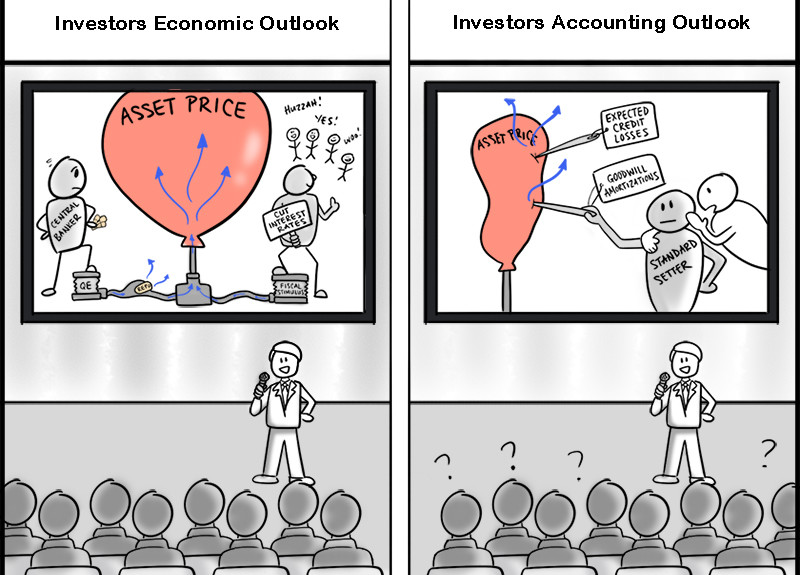

Accounting Requires Standards, Not Accommodation

Accounting standard setters need to revisit the purpose of financial statements. Accommodating broad stakeholders, especially prudential regulators, will not make financial statements increase the transparency for investors and readers. It will only make the information overly complex and increase criticism from advocates of historical cost convention.

Following the 2008 financial crisis, standard setters have become more and more accommodative to regulatory influence. This is concerning and will create significant unintended consequences.

There is no place for ‘prudence’ in modern financial reporting. The accounts of a company should provide ‘neutral’ information that also reflects asset bubbles, market growth trends, volatility, cyclicality and crises as and when they are unfolding. This neutrality will help policymakers to correctly see the trends, diagnose the problems and craft solutions.

Policymakers and regulators are welcome to introduce new rules to regulate capital requirements. At a minimum, the distributable reserves could be updated, and maximum prudential adjustments could be made as regulators deem fit. For instance, the regulators could require immediate write-off of all intangibles and the inclusion of a provision for future expected losses. These regulatory adjustments and disclosures should address ‘prudence’ but take note: tight prudential policies could discourage listings in the local stock exchanges, perhaps one of many unintended consequences.

Investors would benefit from both neutral financial statements and prudent regulatory disclosures

Investors would benefit from both sets of information: neutral financial statements and prudent regulatory disclosures. Financial reporting trying to achieve ‘neutrality’ and ‘prudence’ distorts reality and is helpful to no one.

Nowhere is the challenge associated with accounting hewed to the purposes of regulators and standard setters more pronounced than in goodwill accounting. Currently goodwill accounting, which uses impairment testing, provides a basis to assess the premium paid for an asset. In this construct, rote amortization serves no purpose and artificially deflates a balance sheet regardless of the economic reality. We believe amortization will detect from decision-useful information and instead add opacity surrounding the performance of the acquired businesses.

Without doubt, impairment accounting tends to be less timely. However, the timeliness of impairments could improve overtime with the increased availability of data and willingness to use data analytics along with pending reforms in the audit sector.

In contrast to impairment accounting, amortization of goodwill does not enable investors to differentiate between good managers who make good investments with bad managers who make bad investments. Net, net, amortization removes the constructive pressure on management, auditors and others responsible for recognizing impairments. This is critical since, accounting aside, impairments always catch up with reality

Standard setters should avoid artificially deflating asset bubbles via financial reporting

A recent Financial Times article, suggested that recent merger and acquisition (M&A) spree was encouraged by goodwill capitalization. If we follow this logic, then a replacement rule to immediately write off all intangibles should encourage demergers?

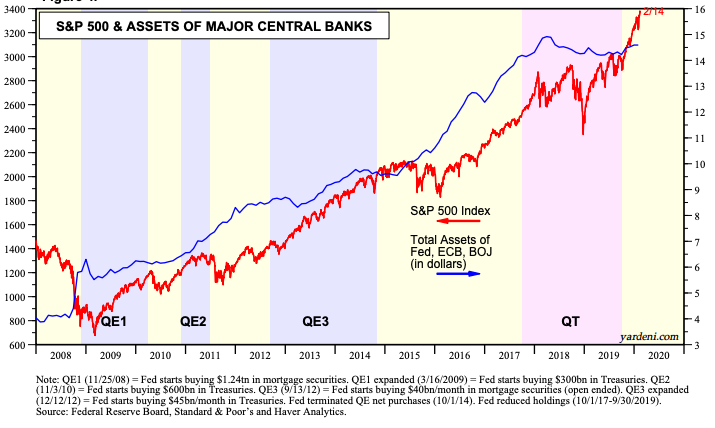

The post-financial crisis rally is mainly, if not entirely, the result of central banks loose monetary policy. The M&A and share buybacks are just tools to inflate the asset bubble (see figures 1 and 2).

Figure 1: S&P 500 & Assets of Major Central Banks

Source: Yardeni Research, Inc.

Figure 2: S&P 500 Shareholders Returns and Goodwill Build-up

Source: FactSet, CFA Institute

The re-introduction of goodwill, as well as the recently promulgated accounting for expected credit losses is a move into uncharted territory. Standard setters should avoid artificially deflating asset bubbles via financial reporting, which they did not create, and thus cannot remedy and instead, push back on prudential regulatory influence and revert to neutrality. For their part, investors supporting ‘prudence’ in general and goodwill amortization in specific, need to rethink whether simplifying accounting at the expense of transparency worth the risk.

Editor’s note: A longer version of this article was first published on Accountingweb 25 February 2020.

Image (c) CFA Institute

Read your article on ‘Audits are not meeting investor expectations’ as well. As mentioned, there should be a lot of catching up on the standard update lines for the standard setters and of course the right implementation by Chartered Accountants, CPAs, the professional bodies and other auditors.