India’s Broking Scandal and Its Aftermath Has Implications for Market Integrity and Efficiency

Late last year, Karvy Broking, one of the largest Indian brokerages with more than 250,000 accounts, was implicated for borrowing against client securities worth at least $267 million and transferring the proceeds to its realty arm.

Indian brokers typically ask for a power-of-attorney mandate from clients to execute sell orders or to create a lien on securities to meet margin requirements. In either case, the securities are transferred from the client’s account to the broker’s account, before the trades are finally settled. In this instance, Karvy abused the mandate by pledging clients’ securities in its account as collateral to borrow from a host of banks and non-banking financial companies.

Some regulatory context is in order. The Securities and Exchange Board of India (SEBI) Depository and Participants Regulations (1996) had long allowed brokers to create a lien on client securities to the extent they are owed and to further create a pledge on them. In June 2019, SEBI replaced this system with a system of segregated accounts for both unpaid sell orders and one created for meeting margin requirements; disallowed brokers from creating pledges on these accounts; and required them to unwind existing pooled accounts to either client accounts upon payment, or sell off, by 31 August 2019.

Most of the brokers sold off their holdings to meet the deadline. Given the tough real estate conditions, however, Karvy couldn’t meet the client commitments by the deadline, delaying pay-outs to clients and attracting regulatory scrutiny, which revealed the scandal. The regulation also revealed the rot in a few other small brokerages that had pledged client securities to fund their proprietary trades.

The aftermath was a mess. SEBI swiftly banned Karvy from taking new clients and removed its power-of-attorney privilege for executing client sell orders. This meant Karvy had to get physical authorization from clients for order execution. SEBI also ordered the depositories to return the pledged securities to client accounts. The aggrieved lenders to Karvy, who had taken the pledged securities as collateral, took their case to the Securities Appellate Tribunal, maintaining they were unaware that the pledged securities were fraudulently transferred from client accounts. The lenders lost their case.

The scandal ushered further reforms. This Feburary, SEBI replaced the system of segregated accounts with a pledge/repledge system, which provides a clear line of sight on the status of pledged securities from client through brokers, that are repledged through clearing members and a clearing corporation. SEBI also required brokerages to collect upfront margins on day trades and asked exchanges to publish margins four times a day. Earlier, clients were getting away without posting the required margin because the margins were determined only at the end of day, whereas brokerages also benefitted from increased turnover. Although SEBI first mooted the implementation date from the end of June, it was twice postponed, first due to the covid-19 lockdown, and later under pressure from brokers.

The brokerage industry has argued that the rules requiring upfront margins would lead to lesser volumes and poorer price discovery. They also have argued that the trading is driven by people who are looking to support their diminished livelihoods.

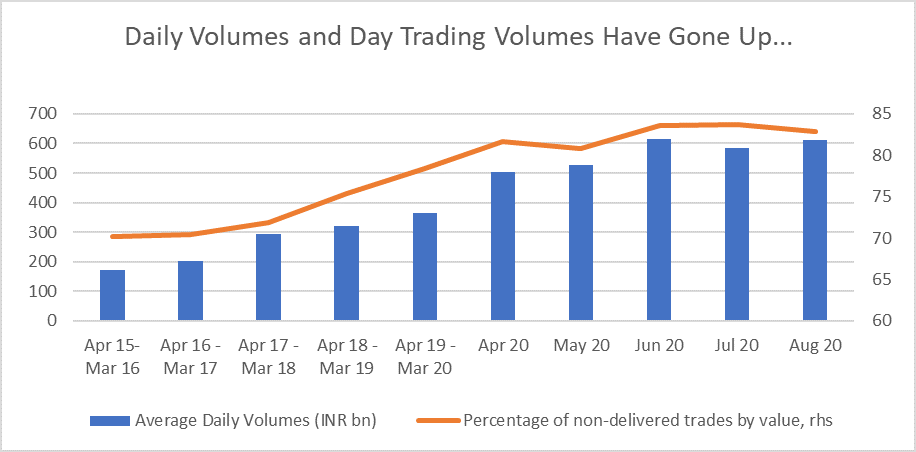

Overall volumes and day-trading volumes have been increasing in recent years, and they reached an all-time high since the beginning of pandemic, mirroring a global trend (figure 1). Average trading value was nearly INR 600 billion in recent months, up from INR 364 in the year ending March 2020. Percentage of trades that were not delivered accounted for nearly 85% of total value, up from 78% in the year ending March 2020.

Figure 1. Daily volumes and day trading

India is also the global leader when it comes to volumes in the derivatives segment, trading 5.96 billion contracts in 2019, compared with 4.83 billion in Chicago Mercantile Exchange (CME).[1]

The rules, which finally went into effect on 1 September 2020, have had a modest impact on trading. Although still in its early days, daily volumes at the National Stock Exchange of India (NSE) have fallen by about 10% since the beginning of September. But any loss in market efficiency needs to be seen against the recent increase in speculative trading activity, and the rules’ intent to protect investors.

The rules, however, also have had a significant unintended impact on client experience, which has varied across brokerages. Leading online brokerages with state-of-the-art systems and early pay-in (shares sold are transferred to the broker’s accounts the same day) have not seen much impact, with the exception that clients cannot use intraday profits to buy new shares before the trades are settled in T+2 days. In contrast, brokerages without early pay-in have had to insist on large upfront margins, even for sale orders. This has generated a lot of consternation among clients. The circular was issued in February, but neither investors nor intermediaries seemed entirely clear about the implications. For example, SEBI, in response to representations from market participants, issued a circular on 15 September 2020 clarifying that only value at risk (VaR) and extreme loss margins (ELM) — about 22% for the median stock — should be collected. “Other margins” (another 15%) do not need to be collected when pay-in is made by T+2 days, and early pay-ins will not attract any margins.

History — from the move toward dematerialization of accounts to the progressive reduction in settlement days — suggests that the industry and customers will adapt to these new rules, if occasionally in a chaotic fashion. It is almost certain that brokerages will upgrade their risk management systems to provide a seamless experience for clients, or risk losing business. The new rules are positive from an investor protection perspective, and they move the industry forward in terms of clearing and settlement timelines.

Hindsight is twenty-twenty but reveals a few pointers. Unlike most reforms, this one did not go through a consultation process. Even if the regulator’s intent was to push through the changes, they could have taken the opportunity to iron out legitimate wrinkles, such as margining requirements for sell orders. With a consultation process, the timeline for reforms would have been longer in the first place, rather than delayed because of resistance from the broader community. A balance can be struck between showing intent and bringing stakeholders along, and the consultation process is important to maintain that balance.

The industry missed a trick, with the laggards not sufficiently preparing their clients for negative surprises and failing to communicate a clear timeline for adapting to the new rules. As we highlight in our Trust Study, information and transparency in communication is a key component of trust, which had taken a beating following this scandal.

Better communication and preparedness by both the regulator and industry may reduce friction to future reforms.

[1] Abhishek Vishnoi and Ashutosh Joshi, “India Now Has World’s Largest Derivatives Exchange by Volume,” Bloomberg, 21 January 2020, https://www.bloomberg.com/news/articles/2020-01-21/india-now-has-world-s-largest-derivatives-exchange-by-volume

Photo Credit @ Getty Images / RapidEye